Confidential - Do not share without permission

Back

Confidential - Do not share without permission

Back

Performance

-

-

Project Prometheus is a Jeff Bezos-led AI company building AI systems for the physical economy, focused on engineering, manufacturing, robotics, scientific discovery, and industrial automation, with the long-term ambition of using AI to redesign how products like computers, automobiles, and spacecraft are built.

Memo Highlights

Confidential

Do not share

Deck only available via Desktop

Highlights

Project Prometheus is a Jeff Bezos-led AI company focused on applying artificial intelligence to the engineering and manufacturing of physical products, including computers, automobiles, and spacecraft. The company reportedly launched with approximately $6.2B in funding and is now nearing a further $10B financing at an approximately $38B valuation. The opportunity is to build an AI-native platform for the physical economy: models and systems that understand physics, engineering constraints, manufacturing processes, robotics, materials, simulation, and real-world production environments.

While the first wave of AI has largely transformed digital workflows, Prometheus is targeting a much larger and harder category: the design, manufacture, and operation of physical systems. The core investment thesis is that Project Prometheus could become one of the defining companies in “physical AI,” combining frontier AI talent, large-scale capital, proprietary industrial data, and Bezos’ operating playbook around infrastructure, vertical integration, and long-duration compounding.

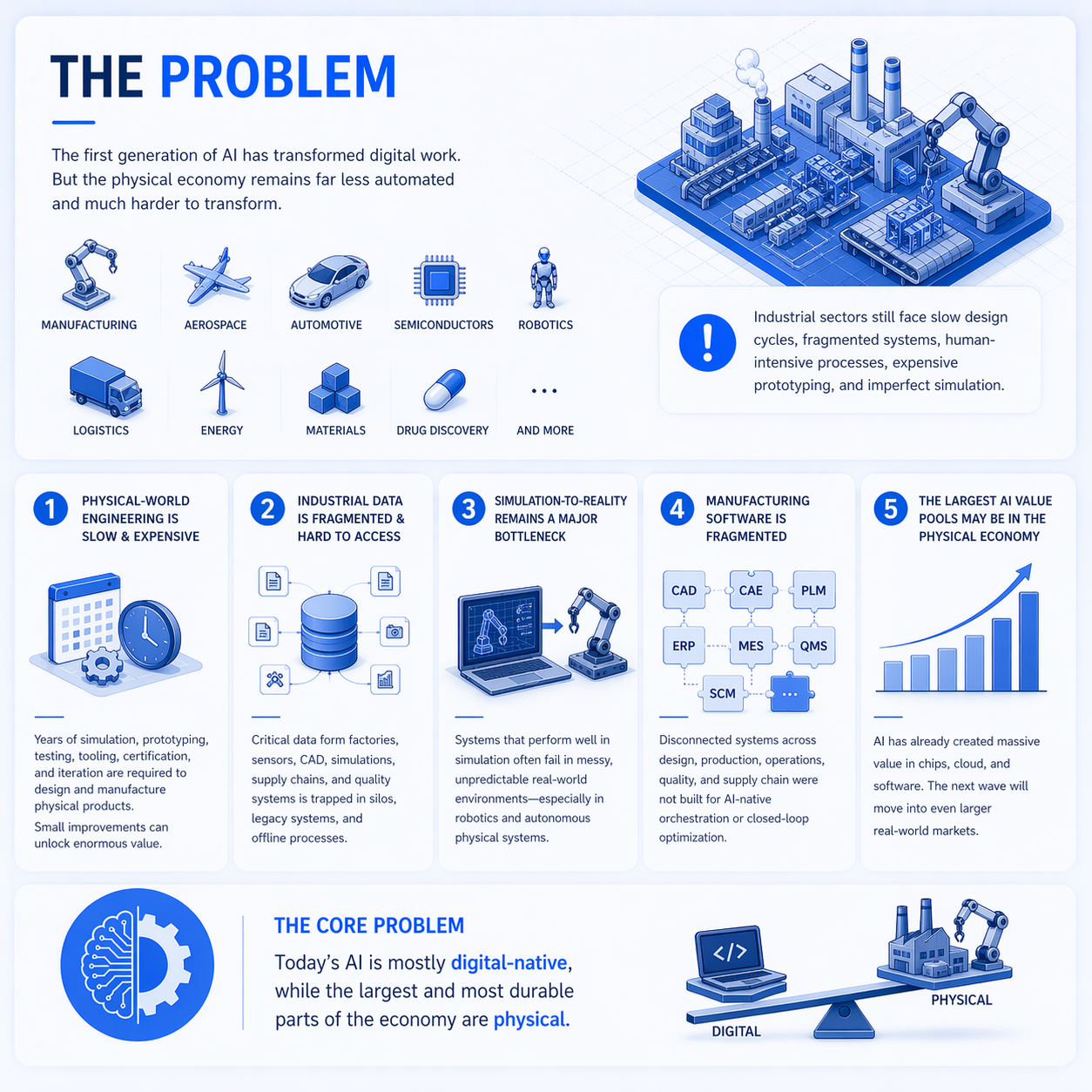

The first generation of generative AI has largely been applied to digital work: writing, coding, search, customer support, productivity, marketing, media generation, and enterprise software. By contrast, the physical economy remains much less automated and significantly harder to transform.

Industrial sectors such as manufacturing, aerospace, automotive, semiconductors, robotics, logistics, energy, materials, and drug discovery still rely on slow design cycles, fragmented software systems, human-intensive processes, expensive prototyping, and imperfect simulation.

The key structural problems are:

Designing and manufacturing a spacecraft, vehicle, robot, chip, battery, aircraft component, or factory line often requires years of simulation, prototyping, physical testing, tooling, certification, and iteration. Even small improvements in cycle time, yield, throughput, failure prediction, or design optimization can create enormous economic value.

Unlike language models, which were trained on massive pools of internet text, physical AI requires proprietary data from factories, robotics systems, CAD files, simulations, sensors, supply chains, materials testing, manufacturing lines, quality-control systems, and real-world production environments. This data is often trapped inside legacy companies, fragmented software stacks, or offline processes.

Robotics and physical AI systems often work well in simulation but fail in messy real-world environments. The broader industry continues to face a significant simulation-to-reality gap, especially in robotics, industrial automation, and autonomous physical systems.

Industrial companies typically operate across disconnected systems: CAD, CAE, PLM, ERP, MES, robotics control software, digital twins, QA systems, warehouse software, supply-chain tools, and human-operated workflows. These systems were not built for AI-native orchestration or closed-loop optimization.

AI has already created enormous value in chips, cloud infrastructure, and software, but the next phase may move into larger physical markets. The AI infrastructure layer has already added hundreds of billions in revenue and trillions in market capitalization, while future competitive arenas are expected to include larger real-world sectors

The core problem is that today’s AI is still mostly digital-native, while the largest and most durable parts of the economy are physical.

Project Prometheus is attempting to build AI for the physical economy. The company is reportedly focused on AI systems that support the engineering and manufacturing of computers, automobiles, and spacecraft, with broader ambitions around robotics, scientific discovery, drug design, and industrial automation.

The company’s solution can be framed as a physical-AI platform or “world lab” that combines:

Models that can reason about physical constraints: materials, motion, heat, stress, airflow, manufacturing tolerances, robotics, energy use, cost, production yield, supply-chain constraints, and real-world failure modes.

Helping engineers design better physical products, including chips, vehicles, aircraft, spacecraft, robotics systems, components, factories, and production processes.

AI to optimize production lines, factory throughput, defect detection, quality control, predictive maintenance, inventory flows, robotics deployment, and supply-chain coordination.

The long-term advantage would be a closed-loop system where simulations generate proposed designs, real-world manufacturing data tests those designs, and the resulting data improves the models. This creates a compounding data advantage that pure software companies may struggle to replicate.

The most differentiated part of the strategy is that Prometheus may not be just a model company. The information provided suggests an ambition to vertically integrate into industrial assets, potentially through partnerships, private equity relationships, and eventually companies owned or influenced by a large Bezos-backed industrial fund. Public reporting has also described Bezos exploring a very large capital pool to acquire and automate manufacturing businesses. If executed, this would make Prometheus more than an AI software vendor. It could become an AI-native industrial operating company: part model lab, part engineering platform, part robotics infrastructure layer, and part industrial conglomerate.

The core insight is that the biggest AI value creation may not come from replacing software workflows, but from rebuilding how physical products are designed, manufactured, distributed, and operated.

Project Prometheus has not publicly disclosed a commercial product, but its likely product architecture can be broken into several layers.

Prometheus may initially focus on AI systems that accelerate engineering simulation and product design. This could include predicting component failure, optimizing airflow, improving thermal performance, reducing material usage, or identifying manufacturability issues earlier in the design process. Public commentary has described potential applications such as software that can predict airflow around an aircraft wing or component failure.

This layer would compete with or augment incumbents in simulation, CAD, CAE, PLM, and digital twins.

A major product direction is likely physical-world modeling: AI systems that understand how objects, machines, robots, and production environments behave over time. The broader market is moving in this direction, with world foundation models increasingly being positioned as core infrastructure for physical AI and robotics.

Prometheus could build a proprietary world lab focused specifically on engineering, manufacturing, robotics, and scientific discovery.

Prometheus reportedly acquired General Agents, an agentic AI company focused on autonomous computer control, shortly after launch. The acquisition suggests that Prometheus may combine physical-world models with agents that can operate software workflows, coordinate engineering tasks, interact with industrial systems, and automate parts of the digital layer around manufacturing. The company reportedly acquired computer-agent capabilities that may be important for orchestrating complex workflows across legacy industrial software.

Over time, Prometheus could extend from design and simulation into robotics, autonomous manufacturing, and industrial control. This could include:

The broader robotics market is already moving toward general-purpose physical AI, with companies and infrastructure providers releasing new physical AI models for next-generation robots.

The most ambitious product vision is an AI-native operating system for industrial companies. This would sit across engineering, simulation, procurement, robotics, production, QA, logistics, and supply-chain operations.

In this scenario, Prometheus would not only sell software. It would help redesign entire industrial companies around AI-native workflows.

If Prometheus is paired with a large industrial acquisition vehicle, the company could deploy its systems inside owned or controlled portfolio companies. That would give it:

This is potentially the company’s strongest moat. A pure software company can sell tools to manufacturers; Prometheus may be able to own or influence the manufacturing environments where the tools are deployed.

The team is the strongest part of the investment case.

Jeff Bezos is reportedly serving as co-CEO of Project Prometheus, marking his first formal operating role since stepping down as Amazon CEO in 2021. He is also reportedly a financial backer of the company, which launched with approximately $6.2B in early funding.

Bezos brings rare credibility across several dimensions:

Prometheus closely fits the Bezos playbook: enter a massive market early, build infrastructure, operate with a long time horizon, vertically integrate, and compound advantages through data, capital, and operational scale.

Vik Bajaj is reportedly co-founder and co-CEO alongside Bezos. He is a physicist and chemist with experience at Google X, Verily, and Foresite Labs. His background is particularly relevant because Prometheus is not simply a consumer AI or enterprise SaaS company; it sits at the intersection of AI, science, engineering, physics, biology, manufacturing, and real-world systems. Bajaj has been described as a scientist and operator with experience in moonshot science and AI-enabled research.

Project Prometheus reportedly recruited approximately 100 employees at launch from leading AI organizations, including OpenAI, DeepMind, and Meta. More recent reporting indicates the company may now have between 50 and 200 employees and is recruiting from OpenAI, Google DeepMind, and xAI.

The company has reportedly hired around 150 engineers and researchers from DeepMind, OpenAI, Google, Meta, Anthropic, and xAI, including one xAI founder.

The team has several important advantages:

The main organizational risk is scope. Prometheus appears to be attempting to build an AI lab, engineering platform, robotics layer, industrial software company, and potentially asset-backed industrial transformation platform at the same time. That ambition creates enormous upside, but also execution risk.

Prometheus is still secretive, so conventional traction metrics such as revenue, customers, gross margin, retention, deployment count, and product usage are not publicly available. However, early traction signals are unusually strong.

The company reportedly launched with approximately $6.2B in funding, making it one of the most heavily funded early-stage startups globally.

Prometheus is reportedly nearing a $10B funding round at an approximately $38B valuation. If completed, this would give the company one of the largest capital bases in private AI.

The company has reportedly recruited from DeepMind, OpenAI, Meta, and more recently has been linked to recruiting from OpenAI, Google DeepMind, and xAI.

Prometheus reportedly acquired General Agents, suggesting it is already using M&A to accelerate capability development rather than relying solely on internal research.

The company’s focus on physical AI places it in one of the most strategically important areas of AI. The industry is rapidly moving toward models and systems that can reason about physical environments, robotics, simulation, manufacturing, and real-world deployment. Broader ecosystem investments in world models and physical AI validate the category.

Project Prometheus is reportedly backed by an unusually large and strategically significant investor base, led in part by Jeff Bezos, who is both a major financial backer and active operating leader of the company. Public reporting also indicates that the company’s new financing includes participation from major institutional investors such as JPMorgan Chase, BlackRock, DST Global, and ARCH Venture Partners. This investor mix is notable because it combines Bezos’ long-term operating capital with large-scale financial institutions and deep technology investors, giving Prometheus access to significant funding, strategic relationships, and credibility as it pursues a highly capital-intensive physical-AI and industrial infrastructure strategy.

Prometheus is targeting one of the largest possible AI markets: the physical economy. Unlike many AI companies focused on software copilots, chat interfaces, or enterprise productivity, Prometheus appears to be pursuing a multi-layer opportunity across engineering, manufacturing, robotics, simulation, scientific discovery, and industrial operations.

Manufacturing remains one of the largest sectors in the global economy, but many workflows remain labor-intensive, fragmented, and under-optimized. AI could create value by improving factory throughput, reducing downtime, improving quality control, optimizing production planning, and enabling more flexible automation.

Engineering simulation, CAD, CAE, PLM, digital twins, and design optimization represent large existing software markets. AI-native tools could compress development cycles and reduce the cost of physical innovation.

Robotics is entering a new phase as models become more general, multimodal, and simulation-trained. Physical AI is increasingly being positioned as the next frontier for robotics, with new models and infrastructure designed to help robots understand and act in real-world environments.

Aerospace and defense are high-value markets where design optimization, autonomy, simulation, manufacturing efficiency, and supply-chain resilience are strategically important. Prometheus’ focus on spacecraft, engineering, and manufacturing fits directly into this category.

Automotive manufacturing involves complex design tradeoffs, software-hardware integration, robotics, supply chains, battery systems, autonomy, and factory optimization. AI-native design and production could materially improve cycle times and cost structures.

Prometheus’ stated focus includes computers, which may include semiconductor design, hardware systems, manufacturing, data centers, thermal optimization, and compute infrastructure. AI could help optimize chip design, packaging, cooling, production yields, and hardware supply chains.

Public descriptions of the company include applications in drug design and scientific discovery. This could expand the addressable market into biology, chemistry, materials science, and AI-driven lab automation.

If paired with a large acquisition fund, Prometheus could capture value not only as a vendor but as an owner/operator of AI-transformed industrial companies. The potential to raise a very large fund to acquire and automate manufacturing companies suggests an asset-backed strategy that could be structurally different from most AI startups.

The market opportunity is not a single TAM. It is a stack of enormous markets:

If Prometheus succeeds, it could become an AI infrastructure layer for the physical economy, analogous to how AWS became infrastructure for the digital economy.

Prometheus faces competition from several categories of companies. Its competitive landscape is broader than traditional AI labs.

Prometheus competes with OpenAI, Google DeepMind, Anthropic, Meta, xAI, and other model companies. These firms are building increasingly capable multimodal, reasoning, coding, and agentic systems. Over time, general-purpose frontier models may become capable enough to perform many engineering, simulation, robotics, and industrial tasks. The risk is that general models become “good enough” for many industrial applications, reducing the need for Prometheus-specific models. Prometheus’ potential edge is specialization: physics, engineering, manufacturing, robotics, proprietary industrial data, and controlled deployment environments.

NVIDIA is both an enabler and a potential competitor. Its hardware powers much of the AI ecosystem, and its software stack is increasingly focused on robotics, simulation, world models, and physical AI. NVIDIA’s Cosmos platform is explicitly designed for world foundation models and physical AI. The risk is that NVIDIA becomes the default physical-AI platform, leaving Prometheus as an application layer. Prometheus’ potential edge is vertical integration, proprietary data, and direct ownership or control of industrial deployment environments.

Tesla has a unique combination of real-world data, robotics, manufacturing experience, autonomy, hardware/software integration, and capital intensity. Its Optimus program and vehicle autonomy efforts create a major embodied-AI data advantage. The risk is that Tesla and xAI become leading players in physical AI through direct deployment in vehicles, factories, and humanoid robots. Prometheus’ potential edge is broader industrial ambition beyond Tesla’s own ecosystem.

Prometheus will compete with entrenched industrial software companies such as Siemens, Dassault Systèmes, Ansys, Autodesk, PTC, Hexagon, Altair, Rockwell Automation, and others.

These companies have deep enterprise relationships, embedded workflows, domain expertise, regulatory familiarity, and high switching costs. The risk is that incumbents integrate AI into existing software stacks before Prometheus can displace or bypass them. Prometheus’ potential edge is being AI-native from inception, unconstrained by legacy architectures.

The robotics field includes Boston Dynamics, Figure AI, Agility Robotics, 1X, Sanctuary AI, Apptronik, Unitree, Skild AI, and others. Some of these companies are building proprietary real-world robot data, hardware platforms, and deployment experience. Robotics companies are increasingly using AI techniques to produce more general-purpose behavior, including collaborations around large behavior models and humanoid robotics.

The risk is that robotics companies own the embodied data layer. Prometheus’ potential edge is that it may not need to own one robot form factor. It could become the intelligence, simulation, and orchestration layer across many types of machines and factories.

Prometheus may also compete with Isomorphic Labs, Xaira Therapeutics, Recursion, Generate Biomedicines, EvolutionaryScale, Insilico Medicine, and others in drug discovery, biology, chemistry, and materials science.

The risk is that specialized science companies move faster in their respective niches. Prometheus’ potential edge is a more generalized physical-world model that can apply across engineering, manufacturing, robotics, chemistry, materials, and biology.

Amazon, Microsoft, Google, Oracle, and other cloud providers control compute, enterprise distribution, AI infrastructure, and customer relationships. They can bundle AI tools into existing enterprise platforms and subsidize adoption. The risk is that hyperscalers become the default AI infrastructure layer for industrial companies. Prometheus’ potential edge is focus, independence, Bezos’ capital network, and a strategy that may combine AI software with physical asset ownership.

Project Prometheus represents a rare opportunity to invest in a potentially category-defining company at the intersection of AI, robotics, engineering, manufacturing, and industrial infrastructure.

The first AI wave has largely transformed digital workflows. The next and potentially larger wave may transform physical systems: factories, robots, vehicles, aircraft, chips, logistics networks, and industrial companies.

Prometheus is positioned directly at this frontier.

Prometheus resembles the strategic pattern behind Amazon and AWS: enter a massive market, invest heavily ahead of demand, build infrastructure, vertically integrate, and compound advantages over long time horizons.

This matters because physical AI will likely require far more capital, patience, operational discipline, and infrastructure than traditional SaaS.

The company’s reported initial $6.2B funding base and potential $10B new round give it the ability to compete aggressively for talent, compute, data, infrastructure, acquisitions, and early deployments. In capital-intensive markets like robotics, simulation, manufacturing, and industrial AI, this matters more than in ordinary software.

If Prometheus obtains data from industrial partners, acquired companies, private equity portfolios, robotics deployments, factories, and engineering systems, it could build a compounding data advantage that general-purpose AI labs cannot easily replicate.

The most differentiated upside case is that Prometheus does not merely sell AI tools to industrial companies. Instead, it may help own, operate, or transform industrial businesses directly. This creates a path to capture both software economics and operational upside.

Prometheus sits at the intersection of AI leadership, manufacturing resilience, robotics, aerospace, defense, reshoring, supply-chain security, and industrial policy. This could make it strategically important to governments, large corporations, and capital providers.

Project Prometheus is one of the most ambitious AI companies in the market. The company is not best understood as another chatbot or enterprise AI startup. It is attempting to build AI for the physical economy: engineering, manufacturing, robotics, simulation, scientific discovery, and industrial operations.

The bull case is extraordinary. If Prometheus can combine frontier AI models, proprietary industrial data, real-world deployment loops, robotics, simulation, and vertical integration, it could become a foundational infrastructure company for the next era of industrial transformation.

The bear case is the company is early, secretive, highly valued, technically ambitious, and entering markets with long deployment cycles and powerful incumbents. The investment case ultimately depends on whether Bezos and Bajaj can convert massive capital, elite talent, and strategic ambition into a proprietary physical-AI platform before the major AI labs, hyperscalers, industrial incumbents, and robotics companies converge on the same opportunity.

Bottom line: Project Prometheus believes AI’s greatest value creation will not be limited to software, but will come from rebuilding the physical economy.

Memo

Project Prometheus is a Jeff Bezos-led AI company focused on applying artificial intelligence to the engineering and manufacturing of physical products, including computers, automobiles, and spacecraft. The company reportedly launched with approximately $6.2B in funding and is now nearing a further $10B financing at an approximately $38B valuation. The opportunity is to build an AI-native platform for the physical economy: models and systems that understand physics, engineering constraints, manufacturing processes, robotics, materials, simulation, and real-world production environments.

While the first wave of AI has largely transformed digital workflows, Prometheus is targeting a much larger and harder category: the design, manufacture, and operation of physical systems. The core investment thesis is that Project Prometheus could become one of the defining companies in “physical AI,” combining frontier AI talent, large-scale capital, proprietary industrial data, and Bezos’ operating playbook around infrastructure, vertical integration, and long-duration compounding.

The first generation of generative AI has largely been applied to digital work: writing, coding, search, customer support, productivity, marketing, media generation, and enterprise software. By contrast, the physical economy remains much less automated and significantly harder to transform.

Industrial sectors such as manufacturing, aerospace, automotive, semiconductors, robotics, logistics, energy, materials, and drug discovery still rely on slow design cycles, fragmented software systems, human-intensive processes, expensive prototyping, and imperfect simulation.

The key structural problems are:

Designing and manufacturing a spacecraft, vehicle, robot, chip, battery, aircraft component, or factory line often requires years of simulation, prototyping, physical testing, tooling, certification, and iteration. Even small improvements in cycle time, yield, throughput, failure prediction, or design optimization can create enormous economic value.

Unlike language models, which were trained on massive pools of internet text, physical AI requires proprietary data from factories, robotics systems, CAD files, simulations, sensors, supply chains, materials testing, manufacturing lines, quality-control systems, and real-world production environments. This data is often trapped inside legacy companies, fragmented software stacks, or offline processes.

Robotics and physical AI systems often work well in simulation but fail in messy real-world environments. The broader industry continues to face a significant simulation-to-reality gap, especially in robotics, industrial automation, and autonomous physical systems.

Industrial companies typically operate across disconnected systems: CAD, CAE, PLM, ERP, MES, robotics control software, digital twins, QA systems, warehouse software, supply-chain tools, and human-operated workflows. These systems were not built for AI-native orchestration or closed-loop optimization.

AI has already created enormous value in chips, cloud infrastructure, and software, but the next phase may move into larger physical markets. The AI infrastructure layer has already added hundreds of billions in revenue and trillions in market capitalization, while future competitive arenas are expected to include larger real-world sectors

The core problem is that today’s AI is still mostly digital-native, while the largest and most durable parts of the economy are physical.

Project Prometheus is attempting to build AI for the physical economy. The company is reportedly focused on AI systems that support the engineering and manufacturing of computers, automobiles, and spacecraft, with broader ambitions around robotics, scientific discovery, drug design, and industrial automation.

The company’s solution can be framed as a physical-AI platform or “world lab” that combines:

Models that can reason about physical constraints: materials, motion, heat, stress, airflow, manufacturing tolerances, robotics, energy use, cost, production yield, supply-chain constraints, and real-world failure modes.

Helping engineers design better physical products, including chips, vehicles, aircraft, spacecraft, robotics systems, components, factories, and production processes.

AI to optimize production lines, factory throughput, defect detection, quality control, predictive maintenance, inventory flows, robotics deployment, and supply-chain coordination.

The long-term advantage would be a closed-loop system where simulations generate proposed designs, real-world manufacturing data tests those designs, and the resulting data improves the models. This creates a compounding data advantage that pure software companies may struggle to replicate.

The most differentiated part of the strategy is that Prometheus may not be just a model company. The information provided suggests an ambition to vertically integrate into industrial assets, potentially through partnerships, private equity relationships, and eventually companies owned or influenced by a large Bezos-backed industrial fund. Public reporting has also described Bezos exploring a very large capital pool to acquire and automate manufacturing businesses. If executed, this would make Prometheus more than an AI software vendor. It could become an AI-native industrial operating company: part model lab, part engineering platform, part robotics infrastructure layer, and part industrial conglomerate.

The core insight is that the biggest AI value creation may not come from replacing software workflows, but from rebuilding how physical products are designed, manufactured, distributed, and operated.

Project Prometheus has not publicly disclosed a commercial product, but its likely product architecture can be broken into several layers.

Prometheus may initially focus on AI systems that accelerate engineering simulation and product design. This could include predicting component failure, optimizing airflow, improving thermal performance, reducing material usage, or identifying manufacturability issues earlier in the design process. Public commentary has described potential applications such as software that can predict airflow around an aircraft wing or component failure.

This layer would compete with or augment incumbents in simulation, CAD, CAE, PLM, and digital twins.

A major product direction is likely physical-world modeling: AI systems that understand how objects, machines, robots, and production environments behave over time. The broader market is moving in this direction, with world foundation models increasingly being positioned as core infrastructure for physical AI and robotics.

Prometheus could build a proprietary world lab focused specifically on engineering, manufacturing, robotics, and scientific discovery.

Prometheus reportedly acquired General Agents, an agentic AI company focused on autonomous computer control, shortly after launch. The acquisition suggests that Prometheus may combine physical-world models with agents that can operate software workflows, coordinate engineering tasks, interact with industrial systems, and automate parts of the digital layer around manufacturing. The company reportedly acquired computer-agent capabilities that may be important for orchestrating complex workflows across legacy industrial software.

Over time, Prometheus could extend from design and simulation into robotics, autonomous manufacturing, and industrial control. This could include:

The broader robotics market is already moving toward general-purpose physical AI, with companies and infrastructure providers releasing new physical AI models for next-generation robots.

The most ambitious product vision is an AI-native operating system for industrial companies. This would sit across engineering, simulation, procurement, robotics, production, QA, logistics, and supply-chain operations.

In this scenario, Prometheus would not only sell software. It would help redesign entire industrial companies around AI-native workflows.

If Prometheus is paired with a large industrial acquisition vehicle, the company could deploy its systems inside owned or controlled portfolio companies. That would give it:

This is potentially the company’s strongest moat. A pure software company can sell tools to manufacturers; Prometheus may be able to own or influence the manufacturing environments where the tools are deployed.

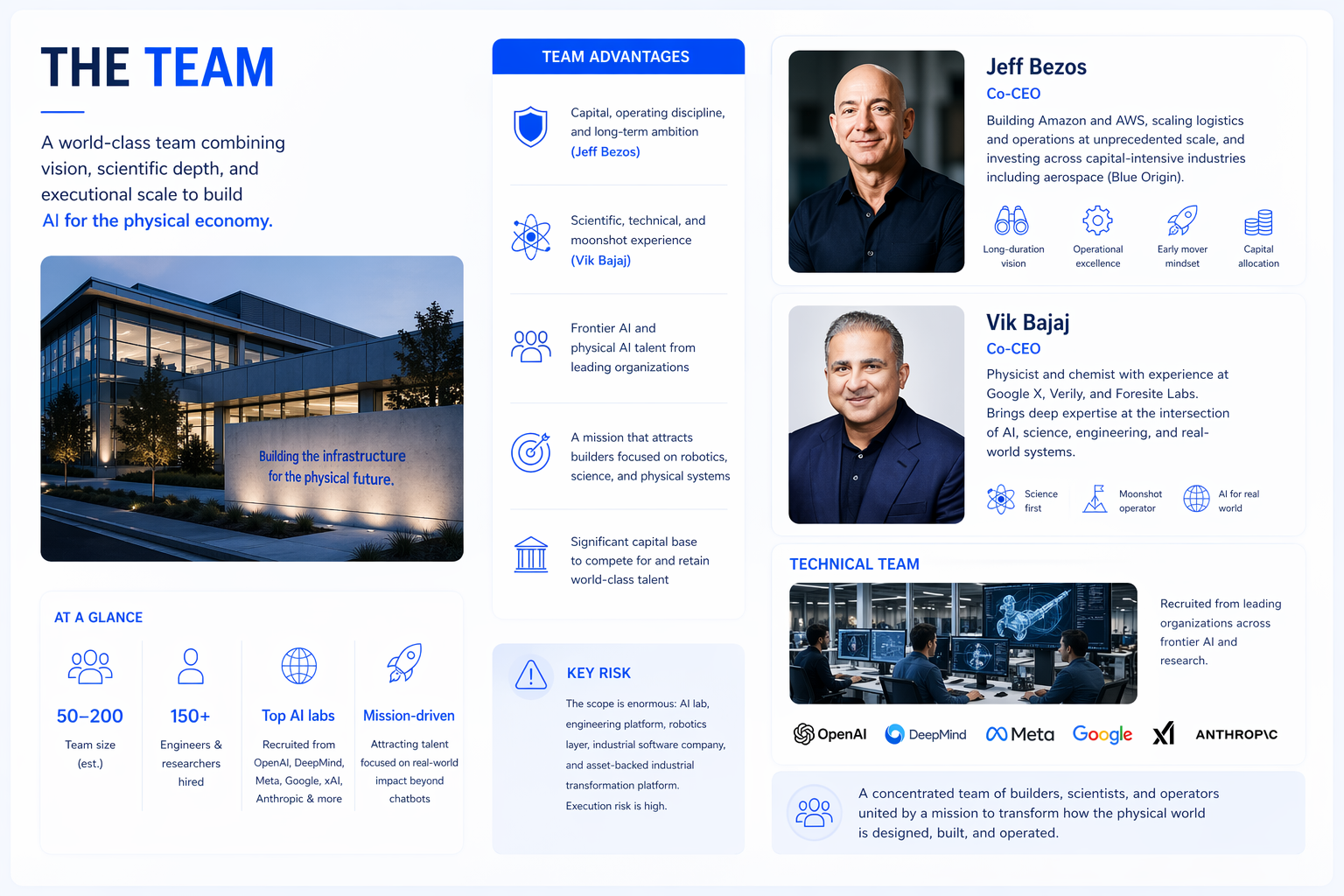

The team is the strongest part of the investment case.

Jeff Bezos is reportedly serving as co-CEO of Project Prometheus, marking his first formal operating role since stepping down as Amazon CEO in 2021. He is also reportedly a financial backer of the company, which launched with approximately $6.2B in early funding.

Bezos brings rare credibility across several dimensions:

Prometheus closely fits the Bezos playbook: enter a massive market early, build infrastructure, operate with a long time horizon, vertically integrate, and compound advantages through data, capital, and operational scale.

Vik Bajaj is reportedly co-founder and co-CEO alongside Bezos. He is a physicist and chemist with experience at Google X, Verily, and Foresite Labs. His background is particularly relevant because Prometheus is not simply a consumer AI or enterprise SaaS company; it sits at the intersection of AI, science, engineering, physics, biology, manufacturing, and real-world systems. Bajaj has been described as a scientist and operator with experience in moonshot science and AI-enabled research.

Project Prometheus reportedly recruited approximately 100 employees at launch from leading AI organizations, including OpenAI, DeepMind, and Meta. More recent reporting indicates the company may now have between 50 and 200 employees and is recruiting from OpenAI, Google DeepMind, and xAI.

The company has reportedly hired around 150 engineers and researchers from DeepMind, OpenAI, Google, Meta, Anthropic, and xAI, including one xAI founder.

The team has several important advantages:

The main organizational risk is scope. Prometheus appears to be attempting to build an AI lab, engineering platform, robotics layer, industrial software company, and potentially asset-backed industrial transformation platform at the same time. That ambition creates enormous upside, but also execution risk.

Prometheus is still secretive, so conventional traction metrics such as revenue, customers, gross margin, retention, deployment count, and product usage are not publicly available. However, early traction signals are unusually strong.

The company reportedly launched with approximately $6.2B in funding, making it one of the most heavily funded early-stage startups globally.

Prometheus is reportedly nearing a $10B funding round at an approximately $38B valuation. If completed, this would give the company one of the largest capital bases in private AI.

The company has reportedly recruited from DeepMind, OpenAI, Meta, and more recently has been linked to recruiting from OpenAI, Google DeepMind, and xAI.

Prometheus reportedly acquired General Agents, suggesting it is already using M&A to accelerate capability development rather than relying solely on internal research.

The company’s focus on physical AI places it in one of the most strategically important areas of AI. The industry is rapidly moving toward models and systems that can reason about physical environments, robotics, simulation, manufacturing, and real-world deployment. Broader ecosystem investments in world models and physical AI validate the category.

Project Prometheus is reportedly backed by an unusually large and strategically significant investor base, led in part by Jeff Bezos, who is both a major financial backer and active operating leader of the company. Public reporting also indicates that the company’s new financing includes participation from major institutional investors such as JPMorgan Chase, BlackRock, DST Global, and ARCH Venture Partners. This investor mix is notable because it combines Bezos’ long-term operating capital with large-scale financial institutions and deep technology investors, giving Prometheus access to significant funding, strategic relationships, and credibility as it pursues a highly capital-intensive physical-AI and industrial infrastructure strategy.

Prometheus is targeting one of the largest possible AI markets: the physical economy. Unlike many AI companies focused on software copilots, chat interfaces, or enterprise productivity, Prometheus appears to be pursuing a multi-layer opportunity across engineering, manufacturing, robotics, simulation, scientific discovery, and industrial operations.

Manufacturing remains one of the largest sectors in the global economy, but many workflows remain labor-intensive, fragmented, and under-optimized. AI could create value by improving factory throughput, reducing downtime, improving quality control, optimizing production planning, and enabling more flexible automation.

Engineering simulation, CAD, CAE, PLM, digital twins, and design optimization represent large existing software markets. AI-native tools could compress development cycles and reduce the cost of physical innovation.

Robotics is entering a new phase as models become more general, multimodal, and simulation-trained. Physical AI is increasingly being positioned as the next frontier for robotics, with new models and infrastructure designed to help robots understand and act in real-world environments.

Aerospace and defense are high-value markets where design optimization, autonomy, simulation, manufacturing efficiency, and supply-chain resilience are strategically important. Prometheus’ focus on spacecraft, engineering, and manufacturing fits directly into this category.

Automotive manufacturing involves complex design tradeoffs, software-hardware integration, robotics, supply chains, battery systems, autonomy, and factory optimization. AI-native design and production could materially improve cycle times and cost structures.

Prometheus’ stated focus includes computers, which may include semiconductor design, hardware systems, manufacturing, data centers, thermal optimization, and compute infrastructure. AI could help optimize chip design, packaging, cooling, production yields, and hardware supply chains.

Public descriptions of the company include applications in drug design and scientific discovery. This could expand the addressable market into biology, chemistry, materials science, and AI-driven lab automation.

If paired with a large acquisition fund, Prometheus could capture value not only as a vendor but as an owner/operator of AI-transformed industrial companies. The potential to raise a very large fund to acquire and automate manufacturing companies suggests an asset-backed strategy that could be structurally different from most AI startups.

The market opportunity is not a single TAM. It is a stack of enormous markets:

If Prometheus succeeds, it could become an AI infrastructure layer for the physical economy, analogous to how AWS became infrastructure for the digital economy.

Prometheus faces competition from several categories of companies. Its competitive landscape is broader than traditional AI labs.

Prometheus competes with OpenAI, Google DeepMind, Anthropic, Meta, xAI, and other model companies. These firms are building increasingly capable multimodal, reasoning, coding, and agentic systems. Over time, general-purpose frontier models may become capable enough to perform many engineering, simulation, robotics, and industrial tasks. The risk is that general models become “good enough” for many industrial applications, reducing the need for Prometheus-specific models. Prometheus’ potential edge is specialization: physics, engineering, manufacturing, robotics, proprietary industrial data, and controlled deployment environments.

NVIDIA is both an enabler and a potential competitor. Its hardware powers much of the AI ecosystem, and its software stack is increasingly focused on robotics, simulation, world models, and physical AI. NVIDIA’s Cosmos platform is explicitly designed for world foundation models and physical AI. The risk is that NVIDIA becomes the default physical-AI platform, leaving Prometheus as an application layer. Prometheus’ potential edge is vertical integration, proprietary data, and direct ownership or control of industrial deployment environments.

Tesla has a unique combination of real-world data, robotics, manufacturing experience, autonomy, hardware/software integration, and capital intensity. Its Optimus program and vehicle autonomy efforts create a major embodied-AI data advantage. The risk is that Tesla and xAI become leading players in physical AI through direct deployment in vehicles, factories, and humanoid robots. Prometheus’ potential edge is broader industrial ambition beyond Tesla’s own ecosystem.

Prometheus will compete with entrenched industrial software companies such as Siemens, Dassault Systèmes, Ansys, Autodesk, PTC, Hexagon, Altair, Rockwell Automation, and others.

These companies have deep enterprise relationships, embedded workflows, domain expertise, regulatory familiarity, and high switching costs. The risk is that incumbents integrate AI into existing software stacks before Prometheus can displace or bypass them. Prometheus’ potential edge is being AI-native from inception, unconstrained by legacy architectures.

The robotics field includes Boston Dynamics, Figure AI, Agility Robotics, 1X, Sanctuary AI, Apptronik, Unitree, Skild AI, and others. Some of these companies are building proprietary real-world robot data, hardware platforms, and deployment experience. Robotics companies are increasingly using AI techniques to produce more general-purpose behavior, including collaborations around large behavior models and humanoid robotics.

The risk is that robotics companies own the embodied data layer. Prometheus’ potential edge is that it may not need to own one robot form factor. It could become the intelligence, simulation, and orchestration layer across many types of machines and factories.

Prometheus may also compete with Isomorphic Labs, Xaira Therapeutics, Recursion, Generate Biomedicines, EvolutionaryScale, Insilico Medicine, and others in drug discovery, biology, chemistry, and materials science.

The risk is that specialized science companies move faster in their respective niches. Prometheus’ potential edge is a more generalized physical-world model that can apply across engineering, manufacturing, robotics, chemistry, materials, and biology.

Amazon, Microsoft, Google, Oracle, and other cloud providers control compute, enterprise distribution, AI infrastructure, and customer relationships. They can bundle AI tools into existing enterprise platforms and subsidize adoption. The risk is that hyperscalers become the default AI infrastructure layer for industrial companies. Prometheus’ potential edge is focus, independence, Bezos’ capital network, and a strategy that may combine AI software with physical asset ownership.

Project Prometheus represents a rare opportunity to invest in a potentially category-defining company at the intersection of AI, robotics, engineering, manufacturing, and industrial infrastructure.

The first AI wave has largely transformed digital workflows. The next and potentially larger wave may transform physical systems: factories, robots, vehicles, aircraft, chips, logistics networks, and industrial companies.

Prometheus is positioned directly at this frontier.

Prometheus resembles the strategic pattern behind Amazon and AWS: enter a massive market, invest heavily ahead of demand, build infrastructure, vertically integrate, and compound advantages over long time horizons.

This matters because physical AI will likely require far more capital, patience, operational discipline, and infrastructure than traditional SaaS.

The company’s reported initial $6.2B funding base and potential $10B new round give it the ability to compete aggressively for talent, compute, data, infrastructure, acquisitions, and early deployments. In capital-intensive markets like robotics, simulation, manufacturing, and industrial AI, this matters more than in ordinary software.

If Prometheus obtains data from industrial partners, acquired companies, private equity portfolios, robotics deployments, factories, and engineering systems, it could build a compounding data advantage that general-purpose AI labs cannot easily replicate.

The most differentiated upside case is that Prometheus does not merely sell AI tools to industrial companies. Instead, it may help own, operate, or transform industrial businesses directly. This creates a path to capture both software economics and operational upside.

Prometheus sits at the intersection of AI leadership, manufacturing resilience, robotics, aerospace, defense, reshoring, supply-chain security, and industrial policy. This could make it strategically important to governments, large corporations, and capital providers.

Project Prometheus is one of the most ambitious AI companies in the market. The company is not best understood as another chatbot or enterprise AI startup. It is attempting to build AI for the physical economy: engineering, manufacturing, robotics, simulation, scientific discovery, and industrial operations.

The bull case is extraordinary. If Prometheus can combine frontier AI models, proprietary industrial data, real-world deployment loops, robotics, simulation, and vertical integration, it could become a foundational infrastructure company for the next era of industrial transformation.

The bear case is the company is early, secretive, highly valued, technically ambitious, and entering markets with long deployment cycles and powerful incumbents. The investment case ultimately depends on whether Bezos and Bajaj can convert massive capital, elite talent, and strategic ambition into a proprietary physical-AI platform before the major AI labs, hyperscalers, industrial incumbents, and robotics companies converge on the same opportunity.

Bottom line: Project Prometheus believes AI’s greatest value creation will not be limited to software, but will come from rebuilding the physical economy.