Confidential - Do not share without permission

Back

Confidential - Do not share without permission

Back

Performance

-

-

Panthalassa is building a new category of AI infrastructure: autonomous ocean nodes that generate clean power from waves, use that power onboard for AI inference, and transmit results back via satellite.

Memo Highlights

Confidential

Do not share

Deck only available via Desktop

Highlights

Panthalassa is building a new category of AI infrastructure: autonomous ocean nodes that generate clean power from waves, use that power onboard for AI inference, and transmit results back via satellite. The company’s core insight is highly compelling: rather than trying to move offshore energy back to land through expensive subsea cables, Panthalassa moves compute to the energy source.

Each node integrates renewable power generation, AI hardware, cooling, propulsion and satellite communications. Instead of transmitting power back to shore, the nodes consume it locally, sending only inference tokens via satellite. The open ocean is one of the few energy resources with tens of terawatts of potential, making it a potentially meaningful new geography for compute and energy infrastructure.

This directly addresses one of the biggest bottlenecks in AI, access to cheap, scalable power, while also avoiding many of the land, grid, cooling, water and permitting constraints facing terrestrial data centers. After a decade of development, Panthalassa has validated multiple prototypes at sea, is building a pilot manufacturing facility, and recently raised a $140M Series B led by Peter Thiel. If Ocean-3 proves the system can operate reliably and the company can scale manufacturing, Panthalassa could become a foundational platform for distributed AI inference, clean ocean energy, and broader blue-economy applications.

Space-based data center concepts are attracting meaningful capital and attention, but remain much earlier and likely harder to scale than Panthalassa:

However, orbital compute remains challenging given launch cost, radiation, thermal rejection, orbital servicing, chip replacement cycles, constellation coordination and space-to-ground data-backhaul constraints. This provides an opportunity for Panthalassa

The investment thesis rests on six core points.

U.S. data centers consumed 176 TWh in 2023, about 4.4% of U.S. electricity, and could reach 325–580 TWh by 2028, representing 6.7–12% of national electricity use. Data centers could consume 9–17% of U.S. electricity by 2030. The grid is not scaling at the same speed as AI demand. Hyperscalers and AI labs can buy GPUs faster than utilities can build new transmission, generation and interconnection capacity. This creates a growing bottleneck for AI infrastructure projects, particularly in concentrated data-center regions such as Northern Virginia, Texas, Arizona and other power-constrained markets.

A typical data center facility can use up to 5 million gallons of water per day — equivalent to more than 16,000 average U.S. households, just for cooling. Growing clusters of data centers near arid regions, such as Phoenix, already consume hundreds of millions of gallons per year, exacerbating drought conditions. High-density AI workloads are pushing rack densities into the 40–100 kW range and beyond, making liquid cooling increasingly necessary.

Building new terrestrial data centers is becoming more difficult. Local communities resist projects due to noise, water use and ecological impacts. Permitting and interconnection can take months or years, and suitable sites near reliable grid infrastructure are scarce. Each new hyperscale campus also requires billions of dollars in transmission upgrades that are ultimately borne by ratepayers. The average global data-center construction cost rose from $7.7 million to $10.7 million per megawatt between 2020 and 2025, with $11.3 million per MW forecast for 2026. These costs are compounded by supply-chain shortages and long lead times.

Wave energy promises abundant, continuous power but has a long history of unsuccessful startups. Previous devices were tethered to the sea floor and required subsea power cables, making them expensive to install and maintain. Prior wave-energy companies such as Pelamis, Aquamarine Power’s Oyster and Ocean Power Technologies struggled with corrosion, biofouling, storms, maintenance and poor economics. As a result, wave energy remains a niche, with most devices producing little power and requiring subsidies.

Panthalassa’s core innovation is an autonomous node that converts wave motion directly into electricity and uses it onboard to power AI inference hardware. Each node consists of a large floating top section and a slender cylindrical structure extending below the surface. In the interview, management described commercial-scale nodes as roughly 20 meters across and 80 meters long, with expected output ranging from approximately 200 kW to 1 MW per node, depending on node size and deployment region. As waves lift and lower the structure, water is pumped into a pressurized reservoir and released through a single turbine, generating continuous power. The system is designed as a simple, solid-state object that uses wave motion to continuously force water through internal channels and a turbine. The design has almost no moving parts and claims a capacity factor up to 90%, far exceeding offshore wind at 30–40% and onshore solar at roughly 25%. By avoiding subsea cables, the system can operate far from shore where waves are stronger. Management describes the best deployment zones as persistent high-wind, high-wave regions, especially in the southern hemisphere. Potential host and manufacturing countries mentioned in the interview include Australia, New Zealand and Chile, with Australia highlighted as attractive because of its industrial base.

On top of or within the node sits a hermetically sealed server bay that houses GPU-class chips for AI inference. The nodes use ocean wave power onboard to run AI chips, while the surrounding ocean provides cooling. Management frames each node as an integrated energy-and-compute appliance: a sealed, mass-produced unit that generates its own power, cools its own chips, communicates wirelessly and has no dependency on local grid infrastructure beyond satellite connectivity. In the interview, Garth Sheldon-Coulson compared the concept to a giant integrated electronics appliance, effectively a self-powered, ocean-based compute device.

Satellite antennas transmit inference outputs back to users and receive model updates, turning what would be an energy-transmission problem into a data-transmission problem. Instead of sending renewable energy to a land-based data center, the floating nodes directly power onboard AI chips and transmit inference tokens via satellite.

Nodes are designed to be towed offshore horizontally, flipped vertical, and then self-propelled using wave-driven hydrodynamics. In the interview, management said the nodes can move at roughly 1–1.5 knots, or around 30 miles per day, and can be directed toward waypoints or instructed to loiter in patterns. Panthalassa’s fleet models assume nodes may be spaced roughly one kilometer apart, both to avoid energy shadowing and to reduce collision / operational risk. Future marine operations are intended to become increasingly autonomous, with nodes towed, deployed, serviced and retrieved with minimal human intervention.

Nodes are built from plate steel in coastal factories and assembled in weeks. They are designed for mass production and require only a simple turbine, generator, power electronics, coatings, and structural steel. In the interview, management emphasized that the manufacturing process is closer to bending and welding steel than to semiconductor fabrication or battery chemistry. Panthalassa estimates each full-scale node could cost approximately $1M to $1.5M, or roughly $1,500 per kW. The company targets $0.02 per kWh at scale and $3B of capital expenditure per gigawatt of combined power and compute, compared with $10 billion or more for land-based alternatives.

Panthalassa has iterated through several generations of prototypes. Ocean-1 completed sea trials in 2021, and Ocean-2 completed sea trials in 2024, validating hydraulic power, computing, satellite telemetry and solid-state propulsion at sea.

The upcoming Ocean-3 program is expected to be a series / mini-fleet rather than a single unit, with versions such as Ocean-3.1, Ocean-3.2 and Ocean-3.3. In the interview, management described Ocean-3 as a smaller pilot fleet, with nodes under 10 meters across and less than 50 kW per node, designed to validate manufacturing, propulsion, autonomy and integrated compute.

This is an important clarification: Ocean-3 is not primarily about demonstrating maximum power output. It is about generating multiple manufacturing and operating repetitions, proving that the company can assemble, deploy, operate and iterate nodes as a repeatable system. Ocean-3 pilot nodes are expected to be deployed in the northern Pacific in 2026, ahead of targeted commercial deployments in 2027.

Management expects the Ocean-3 series to validate the integrated system in 2026, while the manufacturing line is developed in parallel. If successful, Panthalassa aims to begin producing larger commercial-scale nodes by late 2027, likely for deployment in high-energy southern hemisphere ocean regions. Commercial-scale nodes are expected to be materially larger than Ocean-3, with management describing potential units around 20 meters across and 80 meters long, capable of producing approximately 200 kW to 1 MW per node, depending on size and location. Larger nodes should improve per-node economics, but there is an optimum size for each ocean region based on wavelength, steel usage and power capture efficiency.

Initial nodes are optimized for AI inference because latency and bandwidth requirements are manageable via satellite. Management is not targeting frontier model training as the initial use case. Training requires high-speed, low-latency interconnects across large clusters. The target is instead hundreds of gigawatts of AI inference, where input and output data are small relative to the energy consumed by computation. This distinction is critical. The system does not need to replace land-based training clusters to be valuable. It needs to support commercially useful inference workloads where the data rate per unit of energy consumed is low enough for satellite or future fiber-backhauled communications to work. Panthalassa’s original roadmap included high-energy compute applications such as Bitcoin mining, followed by AI and later synthetic fuels. Management argues that compute was always part of the roadmap because it is a natural use case for remote, low-cost energy where moving data is easier than moving electrons.

Nodes rely initially on low-Earth-orbit satellite constellations for high-bandwidth, low-latency communication. Satellite links may be feasible for real-time inference responses but could be limiting for frequent inter-node coordination or large-volume data transfer. While the first architecture relies on LEO satellite connectivity, management also views fiber-backhauled ocean buoys as a potential future option. Under this model, nearby nodes could communicate via radio mesh, with aggregated traffic routed back through a fiber-connected buoy. This reduces perceived satellite-only dependency over time. The company is designing orchestration software to coordinate fleets of nodes, manage power budgets, schedule inference jobs and dispatch data back to terrestrial customers.

Panthalassa has spent the past decade developing its core power generation, propulsion, autonomy and at-sea computing technologies. Ocean-1 and Ocean-2 prototypes matched simulations during sea trials and demonstrated hydraulic power generation, onboard ASIC compute and satellite telemetry. The company also built the Wavehopper test rig in 2024 to optimize fluid dynamics, propulsion and power electronics.

According to the interview, Ocean-1 included both hydrogen production and compute systems, Ocean-2 focused on compute, and Wavehopper validated propulsion. This progression supports the view that Panthalassa is not simply pivoting opportunistically to AI; rather, compute and fuels were long-standing applications for a remote energy platform.

Panthalassa is building a pilot manufacturing facility near Portland, Oregon, funded by its Series B round. The Series B proceeds will help complete the pilot manufacturing facility and accelerate deployment of Ocean-3 nodes. In the interview, management described the manufacturing process as highly parallelizable and based on relatively simple capital equipment: steel rolling, alignment, automated welding, coatings, turbines, generators and power electronics. The company expects to develop the manufacturing line in parallel with Ocean-3 deployment.

In May 2026, the company raised $140 million in Series B financing led by Peter Thiel, with participation from John Doerr, TIME Ventures, SciFi Ventures, Susquehanna Sustainable Investments, Hanwha Asset Management, Fortescue Ventures, Super Micro Computer, Sozo Ventures, Founders Fund, Gigascale Capital, Lowercarbon Capital and others. The capital will complete the pilot factory and accelerate Ocean-3 deployment.

Panthalassa still needs to validate several major projected milestones: Ocean-3 deployment, AI inference at sea, repeatable manufacturing, low-touch fleet operations, commercial customer demand, and the company’s long-term cost targets of roughly $0.02/kWh, $1–1.5M per node, and $3B per GW of compute-plus-power capacity. In the interview, management said Ocean-3 is expected to be deployed off Washington / Oregon in 2026, while a larger manufacturing plan is developed in parallel. If successful, the company aims to begin producing larger commercial-scale nodes by late 2027. Management also referenced upcoming commercial partnerships expected later in 2026, though these have not yet been publicly disclosed.

The financing round attracted marquee investors and high-profile venture funds, demonstrating confidence in Panthalassa’s technology. Given hyperscaler demand for power-constrained compute, Panthalassa should have a large pool of potential customers if Ocean-3 validates the architecture.

Major U.S. tech companies plan to spend $765 billion on AI datacenters in 2026. Traditional datacenter development cannot keep pace due to power scarcity, permitting delays and local opposition. The resulting bottlenecks create a market for alternative infrastructure.

Data centers could consume up to 17% of U.S. electricity by 2030. Data centers are also creating growing concerns around water use, energy bills and community impact. Panthalassa’s offshore approach offloads load from terrestrial grids, eliminating competition for scarce freshwater and freeing up capacity for residential and industrial users.

Waves off U.S. coasts could provide up to 2.64 trillion kWh per year. Globally, the open ocean offers tens of terawatts of potential power. Panthalassa is one of the first companies attempting to harness this resource at scale without relying on subsea export cables.

Advances in satellite communications, AI accelerator efficiency, power electronics, materials science and autonomy now make remote, autonomous infrastructure more feasible. Simulation-driven design has allowed Panthalassa to accelerate iteration and reduce the need for repeated physical wave-tank testing.

Management argues that energy may become a key driver of AI dominance. China is building energy capacity rapidly, while Western datacenter growth is increasingly constrained by permitting, labor, transmission, grid capacity and supply chains. Panthalassa’s model is strategically relevant because it offers a Western-controlled, mass-manufacturable, low-carbon energy and compute platform that does not rely heavily on Chinese solar, battery or inverter supply chains.

Panthalassa’s team combines deep expertise in finance, fluid dynamics, AI hardware, naval architecture and autonomous systems.

Garth Sheldon-Coulson – Co-founder & CEO

Garth is a former Bridgewater Associates strategist with degrees from MIT and Harvard. He leads overall strategy and commercialization, and has guided Panthalassa from lab prototypes to full-scale ocean trials. Investor materials describe him as the de facto architect of the energy-plus-compute platform, with strong analytical ability, recruiting strength and investor references. In the interview, Garth frames Panthalassa as a first-principles response to the question of where humanity can access tens of terawatts of new energy.

Brian Moffat – Co-founder & Chief Innovation Officer

Brian is the company’s technical co-founder and core inventor. He is reportedly associated with 27 patent families and has worked across AI research, Disney Imagineering, Google, computer vision and naval-surveillance concepts. He co-invented core Panthalassa technologies including the Venturi Device, Inertial Hydrodynamic Pump, Wave Engine and solid-state propulsion. In the interview, Garth describes meeting Brian after discovering a YouTube talk in which Brian analyzed prior wave-energy failures and presented early concepts for solid-state ocean energy capture.

Dan Place – Co-director of Node Program / Director of Mechanical Engineering

Dan leads mechanical and structural design, testing, marine operations and prototyping. He has a naval architecture and marine engineering background from the University of Michigan, with prior experience across shipyards, marine test labs, Deepwater Horizon salvage, Boeing UUV work and SpaceX recovery operations. In the interview, Garth notes that Dan was the company’s first hire and had previously worked at SpaceX on drone ship engineering.

The Broader Team - Includes engineers and operators from SpaceX, Google, Blue Origin, Apple, Boeing, NASA, Raytheon, Los Alamos and naval architecture / marine engineering organizations. The company’s team mix appears unusually well matched to the problem, combining hydrodynamics, manufacturing, autonomy, compute, power electronics, satellite communications and offshore operations. The company’s advisory board and investors include Peter Thiel, John Doerr, TIME Ventures and Lowercarbon Capital, bringing networks and capital to support commercialization.

Panthalassa initially targets AI inference workloads. This is the most logical wedge because inference can be more distributed than model training and may tolerate satellite-based communications for a meaningful subset of workloads. The serviceable obtainable market includes cloud providers, enterprise inference customers and AI startups that require large-scale inference but cannot secure enough grid-connected capacity. The near-term customer proposition is not “replace all datacenters,” but rather “provide incremental power-constrained inference capacity where conventional datacenter development is too slow, expensive or politically constrained.”

If Ocean-3 validates the architecture, Panthalassa could build distributed fleets of ocean-based compute nodes for hyperscalers, governments and enterprise AI customers. These fleets would offer compute capacity that is geographically flexible, independent of terrestrial grid interconnection, and cooled naturally by seawater. Major U.S. tech companies plan to spend $765 billion on AI datacenters in 2026. The modular datacenter market averages $10.7 million per MW of construction cost and is forecast to rise to $11.3 million per MW in 2026. US datacenter IT capacity could grow from 35–44 GW in 2024 to 56–132 GW by 2030.

Wave-power potential off American coasts is estimated at 2.64 trillion kWh. By operating far from shore, Panthalassa can access the world’s most energy-dense wave zones and circumvent the permitting, land-use and community impacts that plague terrestrial datacenters. Over time, the platform could serve other high-value workloads such as ocean sensing, maritime surveillance, drone control and synthetic fuel production, including green hydrogen or ammonia. Clean fuels and compute are natural applications for the platform. Government agencies, defense customers, oceanography groups and telecom operators needing remote compute may also become customers.

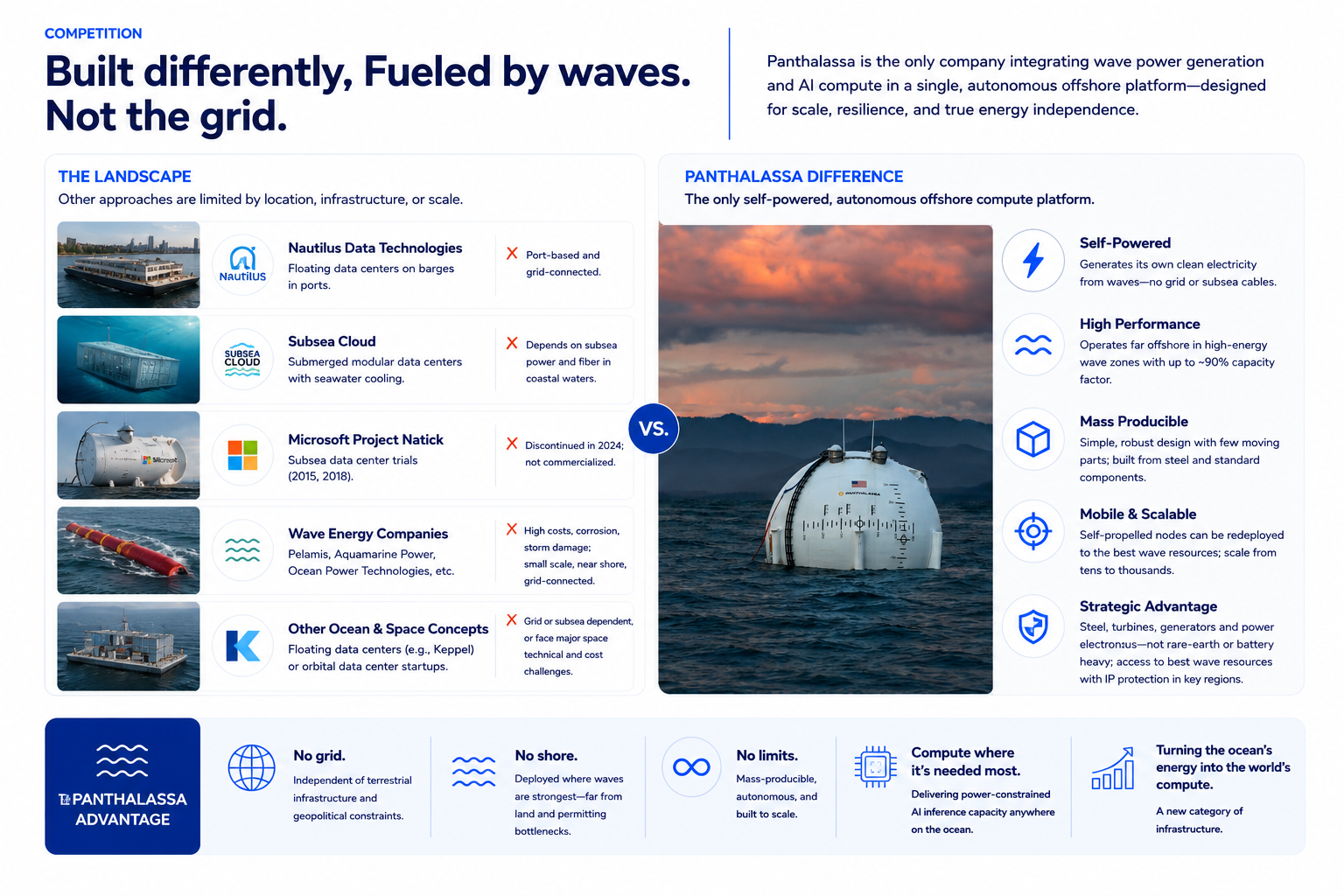

Nautilus Data Technologies: Operates floating datacenters on barges in ports. The facility uses river water cooling and avoids chillers, but remains a port-based, grid-connected datacenter rather than a self-powered offshore compute platform.

Subsea Cloud: Builds submerged modular datacenters. The company’s units are designed for rapid deployment, seawater cooling and large site capacity, but the model depends on subsea power and fiber infrastructure and operates in coastal waters.

Microsoft Project Natick: Microsoft experimented with subsea datacenters in 2015 and 2018. Microsoft confirmed in 2024 that Project Natick was no longer active. While the trial demonstrated that sealed, seawater-cooled systems could operate reliably, Microsoft did not commercialize the concept.

Wave-energy companies: Firms such as Pelamis, Aquamarine Power and Ocean Power Technologies attempted wave-energy converters but struggled with high costs, corrosion and storm damage.

Eco Wave Power and CalWave continue to develop on-shore or near-shore wave devices but require grid connections and produce small amounts of power relative to Panthalassa’s ambition.

Other ocean-compute and space-compute concepts: Companies like Keppel are building floating datacenters connected to the grid. Some startups propose orbital datacenters, but space-based compute faces major challenges around launch cost, radiation, thermal rejection, servicing and data backhaul. Panthalassa may offer some of the same “go where the energy is” advantages with fewer technical hurdles and the ability to retrieve and service nodes.

Panthalassa distinguishes itself by integrating power generation with compute in a single autonomous system. Unlike Nautilus and Subsea Cloud, Panthalassa does not rely on grid electricity or subsea cables. Unlike previous wave-energy startups, its design has few moving parts and operates far offshore, avoiding coastal turbulence and enabling high capacity factors. The ability to mass-produce low-cost nodes, reposition them where waves are strongest, and scale quickly from tens to thousands of units could create a defensible barrier to entry. Panthalassa also has a potential strategic supply-chain advantage. Management argues that the core node is primarily steel, coatings, turbines, generators and power electronics, rather than solar panels, batteries or rare-earth-heavy systems concentrated in China. Management also argues that China lacks direct access to the strongest southern hemisphere wave resources and that Panthalassa has patent coverage in key jurisdictions near those resources.

At $1.7B pre-money, Panthalassa is expensive for a pre-commercial hard-tech company. The round is not priced around prototype novelty alone; it is priced around the possibility that Panthalassa becomes a new category of AI power and compute infrastructure.

The upside case depends on Panthalassa deploying gigawatt-scale offshore compute capacity at a meaningfully lower cost and faster timeline than land-based alternatives. If the company can achieve its target of roughly $3B per GW of combined power-plus-compute capacity, the economics could compare favorably with land-based infrastructure that may exceed $10B per GW when power, datacenter construction, interconnection and permitting are considered.

The return potential becomes compelling if Panthalassa can prove three things: first, that nodes can reliably generate power at sea; second, that they can run commercially useful inference workloads; and third, that customers will pay for offshore compute capacity. If Panthalassa can deploy even a few gigawatts of cost-advantaged compute capacity, the company could justify a valuation many multiples above the current round.

For this investment to work, the following must be true:

Ocean survivability: Panthalassa’s nodes must survive storms, saltwater, corrosion, biofouling, fatigue and long-duration exposure in one of the harshest operating environments on earth. Prior wave-energy companies failed in part because the ocean punished systems that worked well in models and prototypes.

Reliability and maintenance: The business model depends on low-touch or autonomous operation. If nodes require frequent retrieval, inspection or repair, logistics costs could destroy the unit economics.

Manufacturing: Manufacturing is the area management identifies as the company’s biggest remaining execution risk. Although the process is expected to be simpler than batteries or semiconductors, primarily bending and welding steel, Panthalassa has not yet mass-produced nodes at commercial scale. Achieving the targeted $1–1.5 million per node cost will require disciplined manufacturing, supply-chain execution and quality control.

Compute-market fit: Satellite-linked AI inference may work for some workloads, but it is unlikely to replace low-latency, fiber-connected training clusters. The market opportunity depends on identifying inference workloads that are valuable, latency-tolerant and bandwidth-light enough for offshore compute.

Customer: Public materials do not yet disclose signed commercial customers or long-term contracts. Panthalassa must prove not only that the technology works, but that hyperscalers, AI labs or enterprise customers will trust offshore compute for production workloads.

Valuation risk: The $1.7B pre-money valuation leaves less margin for error than an earlier-stage deep-tech round. If Ocean-3 is delayed, underperforms or fails to support commercial inference, the investment could face meaningful downside.

Regulatory and insurance: Autonomous offshore infrastructure may face evolving regulatory frameworks around maritime safety, navigation, environmental impact, data security, international waters and insurance. These issues could affect deployment speed, operating costs and fleet scalability.

Environmental risk: Management argues that the nodes are relatively benign versus other offshore energy systems because they do not touch the seafloor, do not require subsea cables, and are primarily floating steel structures. However, the company still needs to study and manage potential issues including acoustic signature, thermal effects, biofouling, habitat creation and maritime safety.

Panthalassa’s nodes are expected to be largely recyclable because they are primarily steel. Management argues that even aggressive deployment scenarios would use only a small fraction of global steel supply and avoid landfill-heavy or chemically complex waste streams. This could be an advantage versus some energy technologies that rely on complex supply chains, scarce minerals, large land footprints or difficult end-of-life recycling. The sustainability case is not only that the power is zero-emission, but also that the infrastructure may be relatively simple, recoverable and recyclable at end of life.

Panthalassa is tackling one of the most pressing infrastructure challenges of the AI era: how to power massive new compute capacity without overwhelming terrestrial grids or communities. Data-center electricity demand may reach 9–17% of U.S. electricity by 2030. Datacenters are also creating growing water, ratepayer and community pressures. Panthalassa’s autonomous nodes harness the vast, untapped power of ocean waves, delivering continuous renewable electricity, free cooling and onboard AI inference in a single package. Prototypes have validated key parts of the architecture, and the $140 million Series B will fund the transition from prototypes to pilot manufacturing and Ocean-3 deployment.

If the company succeeds, it could unlock a scalable, low-cost and resilient alternative to land-based datacenters, opening a new frontier for clean energy and compute. The strongest version of the thesis is that Panthalassa turns energy deployment into a manufacturing problem: factory-build nodes, tow them offshore, flip them vertical, and let them self-propel to high-energy wave regions with limited dependence on land, grid interconnection, water or permitting. However, significant risks remain. Operating in the open ocean is complex: nodes must withstand storms, corrosion and biofouling for decades, and satellite bandwidth may limit multi-node training workloads. Satellite bandwidth, maintenance and scaling remain important open questions. Panthalassa must also prove that mass-produced nodes can achieve their targeted cost, deliver consistently high power output, and attract paying customers.

Round

Prime round to the Series C - $1.7B valuation

Investors

Peter Thiel, John Doerr, Founders Fund, Gigascale, Lowercarbon, Super Micro Computer, Sozo Ventures, Dylan Field

Date

10 June

Questions

team@joinbeyond.coMemo

Panthalassa is building a new category of AI infrastructure: autonomous ocean nodes that generate clean power from waves, use that power onboard for AI inference, and transmit results back via satellite. The company’s core insight is highly compelling: rather than trying to move offshore energy back to land through expensive subsea cables, Panthalassa moves compute to the energy source.

Each node integrates renewable power generation, AI hardware, cooling, propulsion and satellite communications. Instead of transmitting power back to shore, the nodes consume it locally, sending only inference tokens via satellite. The open ocean is one of the few energy resources with tens of terawatts of potential, making it a potentially meaningful new geography for compute and energy infrastructure.

This directly addresses one of the biggest bottlenecks in AI, access to cheap, scalable power, while also avoiding many of the land, grid, cooling, water and permitting constraints facing terrestrial data centers. After a decade of development, Panthalassa has validated multiple prototypes at sea, is building a pilot manufacturing facility, and recently raised a $140M Series B led by Peter Thiel. If Ocean-3 proves the system can operate reliably and the company can scale manufacturing, Panthalassa could become a foundational platform for distributed AI inference, clean ocean energy, and broader blue-economy applications.

Space-based data center concepts are attracting meaningful capital and attention, but remain much earlier and likely harder to scale than Panthalassa:

However, orbital compute remains challenging given launch cost, radiation, thermal rejection, orbital servicing, chip replacement cycles, constellation coordination and space-to-ground data-backhaul constraints. This provides an opportunity for Panthalassa

The investment thesis rests on six core points.

U.S. data centers consumed 176 TWh in 2023, about 4.4% of U.S. electricity, and could reach 325–580 TWh by 2028, representing 6.7–12% of national electricity use. Data centers could consume 9–17% of U.S. electricity by 2030. The grid is not scaling at the same speed as AI demand. Hyperscalers and AI labs can buy GPUs faster than utilities can build new transmission, generation and interconnection capacity. This creates a growing bottleneck for AI infrastructure projects, particularly in concentrated data-center regions such as Northern Virginia, Texas, Arizona and other power-constrained markets.

A typical data center facility can use up to 5 million gallons of water per day — equivalent to more than 16,000 average U.S. households, just for cooling. Growing clusters of data centers near arid regions, such as Phoenix, already consume hundreds of millions of gallons per year, exacerbating drought conditions. High-density AI workloads are pushing rack densities into the 40–100 kW range and beyond, making liquid cooling increasingly necessary.

Building new terrestrial data centers is becoming more difficult. Local communities resist projects due to noise, water use and ecological impacts. Permitting and interconnection can take months or years, and suitable sites near reliable grid infrastructure are scarce. Each new hyperscale campus also requires billions of dollars in transmission upgrades that are ultimately borne by ratepayers. The average global data-center construction cost rose from $7.7 million to $10.7 million per megawatt between 2020 and 2025, with $11.3 million per MW forecast for 2026. These costs are compounded by supply-chain shortages and long lead times.

Wave energy promises abundant, continuous power but has a long history of unsuccessful startups. Previous devices were tethered to the sea floor and required subsea power cables, making them expensive to install and maintain. Prior wave-energy companies such as Pelamis, Aquamarine Power’s Oyster and Ocean Power Technologies struggled with corrosion, biofouling, storms, maintenance and poor economics. As a result, wave energy remains a niche, with most devices producing little power and requiring subsidies.

Panthalassa’s core innovation is an autonomous node that converts wave motion directly into electricity and uses it onboard to power AI inference hardware. Each node consists of a large floating top section and a slender cylindrical structure extending below the surface. In the interview, management described commercial-scale nodes as roughly 20 meters across and 80 meters long, with expected output ranging from approximately 200 kW to 1 MW per node, depending on node size and deployment region. As waves lift and lower the structure, water is pumped into a pressurized reservoir and released through a single turbine, generating continuous power. The system is designed as a simple, solid-state object that uses wave motion to continuously force water through internal channels and a turbine. The design has almost no moving parts and claims a capacity factor up to 90%, far exceeding offshore wind at 30–40% and onshore solar at roughly 25%. By avoiding subsea cables, the system can operate far from shore where waves are stronger. Management describes the best deployment zones as persistent high-wind, high-wave regions, especially in the southern hemisphere. Potential host and manufacturing countries mentioned in the interview include Australia, New Zealand and Chile, with Australia highlighted as attractive because of its industrial base.

On top of or within the node sits a hermetically sealed server bay that houses GPU-class chips for AI inference. The nodes use ocean wave power onboard to run AI chips, while the surrounding ocean provides cooling. Management frames each node as an integrated energy-and-compute appliance: a sealed, mass-produced unit that generates its own power, cools its own chips, communicates wirelessly and has no dependency on local grid infrastructure beyond satellite connectivity. In the interview, Garth Sheldon-Coulson compared the concept to a giant integrated electronics appliance, effectively a self-powered, ocean-based compute device.

Satellite antennas transmit inference outputs back to users and receive model updates, turning what would be an energy-transmission problem into a data-transmission problem. Instead of sending renewable energy to a land-based data center, the floating nodes directly power onboard AI chips and transmit inference tokens via satellite.

Nodes are designed to be towed offshore horizontally, flipped vertical, and then self-propelled using wave-driven hydrodynamics. In the interview, management said the nodes can move at roughly 1–1.5 knots, or around 30 miles per day, and can be directed toward waypoints or instructed to loiter in patterns. Panthalassa’s fleet models assume nodes may be spaced roughly one kilometer apart, both to avoid energy shadowing and to reduce collision / operational risk. Future marine operations are intended to become increasingly autonomous, with nodes towed, deployed, serviced and retrieved with minimal human intervention.

Nodes are built from plate steel in coastal factories and assembled in weeks. They are designed for mass production and require only a simple turbine, generator, power electronics, coatings, and structural steel. In the interview, management emphasized that the manufacturing process is closer to bending and welding steel than to semiconductor fabrication or battery chemistry. Panthalassa estimates each full-scale node could cost approximately $1M to $1.5M, or roughly $1,500 per kW. The company targets $0.02 per kWh at scale and $3B of capital expenditure per gigawatt of combined power and compute, compared with $10 billion or more for land-based alternatives.

Panthalassa has iterated through several generations of prototypes. Ocean-1 completed sea trials in 2021, and Ocean-2 completed sea trials in 2024, validating hydraulic power, computing, satellite telemetry and solid-state propulsion at sea.

The upcoming Ocean-3 program is expected to be a series / mini-fleet rather than a single unit, with versions such as Ocean-3.1, Ocean-3.2 and Ocean-3.3. In the interview, management described Ocean-3 as a smaller pilot fleet, with nodes under 10 meters across and less than 50 kW per node, designed to validate manufacturing, propulsion, autonomy and integrated compute.

This is an important clarification: Ocean-3 is not primarily about demonstrating maximum power output. It is about generating multiple manufacturing and operating repetitions, proving that the company can assemble, deploy, operate and iterate nodes as a repeatable system. Ocean-3 pilot nodes are expected to be deployed in the northern Pacific in 2026, ahead of targeted commercial deployments in 2027.

Management expects the Ocean-3 series to validate the integrated system in 2026, while the manufacturing line is developed in parallel. If successful, Panthalassa aims to begin producing larger commercial-scale nodes by late 2027, likely for deployment in high-energy southern hemisphere ocean regions. Commercial-scale nodes are expected to be materially larger than Ocean-3, with management describing potential units around 20 meters across and 80 meters long, capable of producing approximately 200 kW to 1 MW per node, depending on size and location. Larger nodes should improve per-node economics, but there is an optimum size for each ocean region based on wavelength, steel usage and power capture efficiency.

Initial nodes are optimized for AI inference because latency and bandwidth requirements are manageable via satellite. Management is not targeting frontier model training as the initial use case. Training requires high-speed, low-latency interconnects across large clusters. The target is instead hundreds of gigawatts of AI inference, where input and output data are small relative to the energy consumed by computation. This distinction is critical. The system does not need to replace land-based training clusters to be valuable. It needs to support commercially useful inference workloads where the data rate per unit of energy consumed is low enough for satellite or future fiber-backhauled communications to work. Panthalassa’s original roadmap included high-energy compute applications such as Bitcoin mining, followed by AI and later synthetic fuels. Management argues that compute was always part of the roadmap because it is a natural use case for remote, low-cost energy where moving data is easier than moving electrons.

Nodes rely initially on low-Earth-orbit satellite constellations for high-bandwidth, low-latency communication. Satellite links may be feasible for real-time inference responses but could be limiting for frequent inter-node coordination or large-volume data transfer. While the first architecture relies on LEO satellite connectivity, management also views fiber-backhauled ocean buoys as a potential future option. Under this model, nearby nodes could communicate via radio mesh, with aggregated traffic routed back through a fiber-connected buoy. This reduces perceived satellite-only dependency over time. The company is designing orchestration software to coordinate fleets of nodes, manage power budgets, schedule inference jobs and dispatch data back to terrestrial customers.

Panthalassa has spent the past decade developing its core power generation, propulsion, autonomy and at-sea computing technologies. Ocean-1 and Ocean-2 prototypes matched simulations during sea trials and demonstrated hydraulic power generation, onboard ASIC compute and satellite telemetry. The company also built the Wavehopper test rig in 2024 to optimize fluid dynamics, propulsion and power electronics.

According to the interview, Ocean-1 included both hydrogen production and compute systems, Ocean-2 focused on compute, and Wavehopper validated propulsion. This progression supports the view that Panthalassa is not simply pivoting opportunistically to AI; rather, compute and fuels were long-standing applications for a remote energy platform.

Panthalassa is building a pilot manufacturing facility near Portland, Oregon, funded by its Series B round. The Series B proceeds will help complete the pilot manufacturing facility and accelerate deployment of Ocean-3 nodes. In the interview, management described the manufacturing process as highly parallelizable and based on relatively simple capital equipment: steel rolling, alignment, automated welding, coatings, turbines, generators and power electronics. The company expects to develop the manufacturing line in parallel with Ocean-3 deployment.

In May 2026, the company raised $140 million in Series B financing led by Peter Thiel, with participation from John Doerr, TIME Ventures, SciFi Ventures, Susquehanna Sustainable Investments, Hanwha Asset Management, Fortescue Ventures, Super Micro Computer, Sozo Ventures, Founders Fund, Gigascale Capital, Lowercarbon Capital and others. The capital will complete the pilot factory and accelerate Ocean-3 deployment.

Panthalassa still needs to validate several major projected milestones: Ocean-3 deployment, AI inference at sea, repeatable manufacturing, low-touch fleet operations, commercial customer demand, and the company’s long-term cost targets of roughly $0.02/kWh, $1–1.5M per node, and $3B per GW of compute-plus-power capacity. In the interview, management said Ocean-3 is expected to be deployed off Washington / Oregon in 2026, while a larger manufacturing plan is developed in parallel. If successful, the company aims to begin producing larger commercial-scale nodes by late 2027. Management also referenced upcoming commercial partnerships expected later in 2026, though these have not yet been publicly disclosed.

The financing round attracted marquee investors and high-profile venture funds, demonstrating confidence in Panthalassa’s technology. Given hyperscaler demand for power-constrained compute, Panthalassa should have a large pool of potential customers if Ocean-3 validates the architecture.

Major U.S. tech companies plan to spend $765 billion on AI datacenters in 2026. Traditional datacenter development cannot keep pace due to power scarcity, permitting delays and local opposition. The resulting bottlenecks create a market for alternative infrastructure.

Data centers could consume up to 17% of U.S. electricity by 2030. Data centers are also creating growing concerns around water use, energy bills and community impact. Panthalassa’s offshore approach offloads load from terrestrial grids, eliminating competition for scarce freshwater and freeing up capacity for residential and industrial users.

Waves off U.S. coasts could provide up to 2.64 trillion kWh per year. Globally, the open ocean offers tens of terawatts of potential power. Panthalassa is one of the first companies attempting to harness this resource at scale without relying on subsea export cables.

Advances in satellite communications, AI accelerator efficiency, power electronics, materials science and autonomy now make remote, autonomous infrastructure more feasible. Simulation-driven design has allowed Panthalassa to accelerate iteration and reduce the need for repeated physical wave-tank testing.

Management argues that energy may become a key driver of AI dominance. China is building energy capacity rapidly, while Western datacenter growth is increasingly constrained by permitting, labor, transmission, grid capacity and supply chains. Panthalassa’s model is strategically relevant because it offers a Western-controlled, mass-manufacturable, low-carbon energy and compute platform that does not rely heavily on Chinese solar, battery or inverter supply chains.

Panthalassa’s team combines deep expertise in finance, fluid dynamics, AI hardware, naval architecture and autonomous systems.

Garth Sheldon-Coulson – Co-founder & CEO

Garth is a former Bridgewater Associates strategist with degrees from MIT and Harvard. He leads overall strategy and commercialization, and has guided Panthalassa from lab prototypes to full-scale ocean trials. Investor materials describe him as the de facto architect of the energy-plus-compute platform, with strong analytical ability, recruiting strength and investor references. In the interview, Garth frames Panthalassa as a first-principles response to the question of where humanity can access tens of terawatts of new energy.

Brian Moffat – Co-founder & Chief Innovation Officer

Brian is the company’s technical co-founder and core inventor. He is reportedly associated with 27 patent families and has worked across AI research, Disney Imagineering, Google, computer vision and naval-surveillance concepts. He co-invented core Panthalassa technologies including the Venturi Device, Inertial Hydrodynamic Pump, Wave Engine and solid-state propulsion. In the interview, Garth describes meeting Brian after discovering a YouTube talk in which Brian analyzed prior wave-energy failures and presented early concepts for solid-state ocean energy capture.

Dan Place – Co-director of Node Program / Director of Mechanical Engineering

Dan leads mechanical and structural design, testing, marine operations and prototyping. He has a naval architecture and marine engineering background from the University of Michigan, with prior experience across shipyards, marine test labs, Deepwater Horizon salvage, Boeing UUV work and SpaceX recovery operations. In the interview, Garth notes that Dan was the company’s first hire and had previously worked at SpaceX on drone ship engineering.

The Broader Team - Includes engineers and operators from SpaceX, Google, Blue Origin, Apple, Boeing, NASA, Raytheon, Los Alamos and naval architecture / marine engineering organizations. The company’s team mix appears unusually well matched to the problem, combining hydrodynamics, manufacturing, autonomy, compute, power electronics, satellite communications and offshore operations. The company’s advisory board and investors include Peter Thiel, John Doerr, TIME Ventures and Lowercarbon Capital, bringing networks and capital to support commercialization.

Panthalassa initially targets AI inference workloads. This is the most logical wedge because inference can be more distributed than model training and may tolerate satellite-based communications for a meaningful subset of workloads. The serviceable obtainable market includes cloud providers, enterprise inference customers and AI startups that require large-scale inference but cannot secure enough grid-connected capacity. The near-term customer proposition is not “replace all datacenters,” but rather “provide incremental power-constrained inference capacity where conventional datacenter development is too slow, expensive or politically constrained.”

If Ocean-3 validates the architecture, Panthalassa could build distributed fleets of ocean-based compute nodes for hyperscalers, governments and enterprise AI customers. These fleets would offer compute capacity that is geographically flexible, independent of terrestrial grid interconnection, and cooled naturally by seawater. Major U.S. tech companies plan to spend $765 billion on AI datacenters in 2026. The modular datacenter market averages $10.7 million per MW of construction cost and is forecast to rise to $11.3 million per MW in 2026. US datacenter IT capacity could grow from 35–44 GW in 2024 to 56–132 GW by 2030.

Wave-power potential off American coasts is estimated at 2.64 trillion kWh. By operating far from shore, Panthalassa can access the world’s most energy-dense wave zones and circumvent the permitting, land-use and community impacts that plague terrestrial datacenters. Over time, the platform could serve other high-value workloads such as ocean sensing, maritime surveillance, drone control and synthetic fuel production, including green hydrogen or ammonia. Clean fuels and compute are natural applications for the platform. Government agencies, defense customers, oceanography groups and telecom operators needing remote compute may also become customers.

Nautilus Data Technologies: Operates floating datacenters on barges in ports. The facility uses river water cooling and avoids chillers, but remains a port-based, grid-connected datacenter rather than a self-powered offshore compute platform.

Subsea Cloud: Builds submerged modular datacenters. The company’s units are designed for rapid deployment, seawater cooling and large site capacity, but the model depends on subsea power and fiber infrastructure and operates in coastal waters.

Microsoft Project Natick: Microsoft experimented with subsea datacenters in 2015 and 2018. Microsoft confirmed in 2024 that Project Natick was no longer active. While the trial demonstrated that sealed, seawater-cooled systems could operate reliably, Microsoft did not commercialize the concept.

Wave-energy companies: Firms such as Pelamis, Aquamarine Power and Ocean Power Technologies attempted wave-energy converters but struggled with high costs, corrosion and storm damage.

Eco Wave Power and CalWave continue to develop on-shore or near-shore wave devices but require grid connections and produce small amounts of power relative to Panthalassa’s ambition.

Other ocean-compute and space-compute concepts: Companies like Keppel are building floating datacenters connected to the grid. Some startups propose orbital datacenters, but space-based compute faces major challenges around launch cost, radiation, thermal rejection, servicing and data backhaul. Panthalassa may offer some of the same “go where the energy is” advantages with fewer technical hurdles and the ability to retrieve and service nodes.

Panthalassa distinguishes itself by integrating power generation with compute in a single autonomous system. Unlike Nautilus and Subsea Cloud, Panthalassa does not rely on grid electricity or subsea cables. Unlike previous wave-energy startups, its design has few moving parts and operates far offshore, avoiding coastal turbulence and enabling high capacity factors. The ability to mass-produce low-cost nodes, reposition them where waves are strongest, and scale quickly from tens to thousands of units could create a defensible barrier to entry. Panthalassa also has a potential strategic supply-chain advantage. Management argues that the core node is primarily steel, coatings, turbines, generators and power electronics, rather than solar panels, batteries or rare-earth-heavy systems concentrated in China. Management also argues that China lacks direct access to the strongest southern hemisphere wave resources and that Panthalassa has patent coverage in key jurisdictions near those resources.

At $1.7B pre-money, Panthalassa is expensive for a pre-commercial hard-tech company. The round is not priced around prototype novelty alone; it is priced around the possibility that Panthalassa becomes a new category of AI power and compute infrastructure.

The upside case depends on Panthalassa deploying gigawatt-scale offshore compute capacity at a meaningfully lower cost and faster timeline than land-based alternatives. If the company can achieve its target of roughly $3B per GW of combined power-plus-compute capacity, the economics could compare favorably with land-based infrastructure that may exceed $10B per GW when power, datacenter construction, interconnection and permitting are considered.

The return potential becomes compelling if Panthalassa can prove three things: first, that nodes can reliably generate power at sea; second, that they can run commercially useful inference workloads; and third, that customers will pay for offshore compute capacity. If Panthalassa can deploy even a few gigawatts of cost-advantaged compute capacity, the company could justify a valuation many multiples above the current round.

For this investment to work, the following must be true:

Ocean survivability: Panthalassa’s nodes must survive storms, saltwater, corrosion, biofouling, fatigue and long-duration exposure in one of the harshest operating environments on earth. Prior wave-energy companies failed in part because the ocean punished systems that worked well in models and prototypes.

Reliability and maintenance: The business model depends on low-touch or autonomous operation. If nodes require frequent retrieval, inspection or repair, logistics costs could destroy the unit economics.

Manufacturing: Manufacturing is the area management identifies as the company’s biggest remaining execution risk. Although the process is expected to be simpler than batteries or semiconductors, primarily bending and welding steel, Panthalassa has not yet mass-produced nodes at commercial scale. Achieving the targeted $1–1.5 million per node cost will require disciplined manufacturing, supply-chain execution and quality control.

Compute-market fit: Satellite-linked AI inference may work for some workloads, but it is unlikely to replace low-latency, fiber-connected training clusters. The market opportunity depends on identifying inference workloads that are valuable, latency-tolerant and bandwidth-light enough for offshore compute.

Customer: Public materials do not yet disclose signed commercial customers or long-term contracts. Panthalassa must prove not only that the technology works, but that hyperscalers, AI labs or enterprise customers will trust offshore compute for production workloads.

Valuation risk: The $1.7B pre-money valuation leaves less margin for error than an earlier-stage deep-tech round. If Ocean-3 is delayed, underperforms or fails to support commercial inference, the investment could face meaningful downside.

Regulatory and insurance: Autonomous offshore infrastructure may face evolving regulatory frameworks around maritime safety, navigation, environmental impact, data security, international waters and insurance. These issues could affect deployment speed, operating costs and fleet scalability.

Environmental risk: Management argues that the nodes are relatively benign versus other offshore energy systems because they do not touch the seafloor, do not require subsea cables, and are primarily floating steel structures. However, the company still needs to study and manage potential issues including acoustic signature, thermal effects, biofouling, habitat creation and maritime safety.

Panthalassa’s nodes are expected to be largely recyclable because they are primarily steel. Management argues that even aggressive deployment scenarios would use only a small fraction of global steel supply and avoid landfill-heavy or chemically complex waste streams. This could be an advantage versus some energy technologies that rely on complex supply chains, scarce minerals, large land footprints or difficult end-of-life recycling. The sustainability case is not only that the power is zero-emission, but also that the infrastructure may be relatively simple, recoverable and recyclable at end of life.

Panthalassa is tackling one of the most pressing infrastructure challenges of the AI era: how to power massive new compute capacity without overwhelming terrestrial grids or communities. Data-center electricity demand may reach 9–17% of U.S. electricity by 2030. Datacenters are also creating growing water, ratepayer and community pressures. Panthalassa’s autonomous nodes harness the vast, untapped power of ocean waves, delivering continuous renewable electricity, free cooling and onboard AI inference in a single package. Prototypes have validated key parts of the architecture, and the $140 million Series B will fund the transition from prototypes to pilot manufacturing and Ocean-3 deployment.

If the company succeeds, it could unlock a scalable, low-cost and resilient alternative to land-based datacenters, opening a new frontier for clean energy and compute. The strongest version of the thesis is that Panthalassa turns energy deployment into a manufacturing problem: factory-build nodes, tow them offshore, flip them vertical, and let them self-propel to high-energy wave regions with limited dependence on land, grid interconnection, water or permitting. However, significant risks remain. Operating in the open ocean is complex: nodes must withstand storms, corrosion and biofouling for decades, and satellite bandwidth may limit multi-node training workloads. Satellite bandwidth, maintenance and scaling remain important open questions. Panthalassa must also prove that mass-produced nodes can achieve their targeted cost, deliver consistently high power output, and attract paying customers.