Confidential - Do not share without permission

Back

Confidential - Do not share without permission

Back

Performance

-

-

Core Automation is an AI lab building automated research systems, with a focus on continual-learning agents and post-transformer architectures. The company’s thesis is that the next major AI breakthrough will come from automating the lab itself: agents running research workflows, generating data, and improving the models that operate the lab.

Memo Highlights

Confidential

Do not share

Deck only available via Desktop

Highlights

Core Automation is a highly credible AI “neo-lab” building “the world’s most automated AI lab,” starting by automating its own research workflows. Founded by former OpenAI VP Jerry Tworek, with senior talent from Anthropic, Google DeepMind, Adept, Meta, and Google, the team is very strong across reasoning models, pretraining, multimodal agents, GPU systems, inference, model behavior, and AI infrastructure.

Rather than building another AI application, Core is creating a self-reinforcing research engine where agents run workflows, generate training data, and improve the models operating the lab. If successful, this could allow a small, talent-dense team to compete with much larger frontier labs while pursuing breakthroughs in continual learning, post-transformer architectures, GPU-kernel automation, and more efficient training.

Core may represent the next phase of AI. While highly ambitious, this is the type of paradigm-shift bet that can define a generation of AI companies, similar in spirit to Anthropic: when Dario Amodei left OpenAI to build a frontier lab, an investment at a $3B valuation would have produced a return of over 300x.

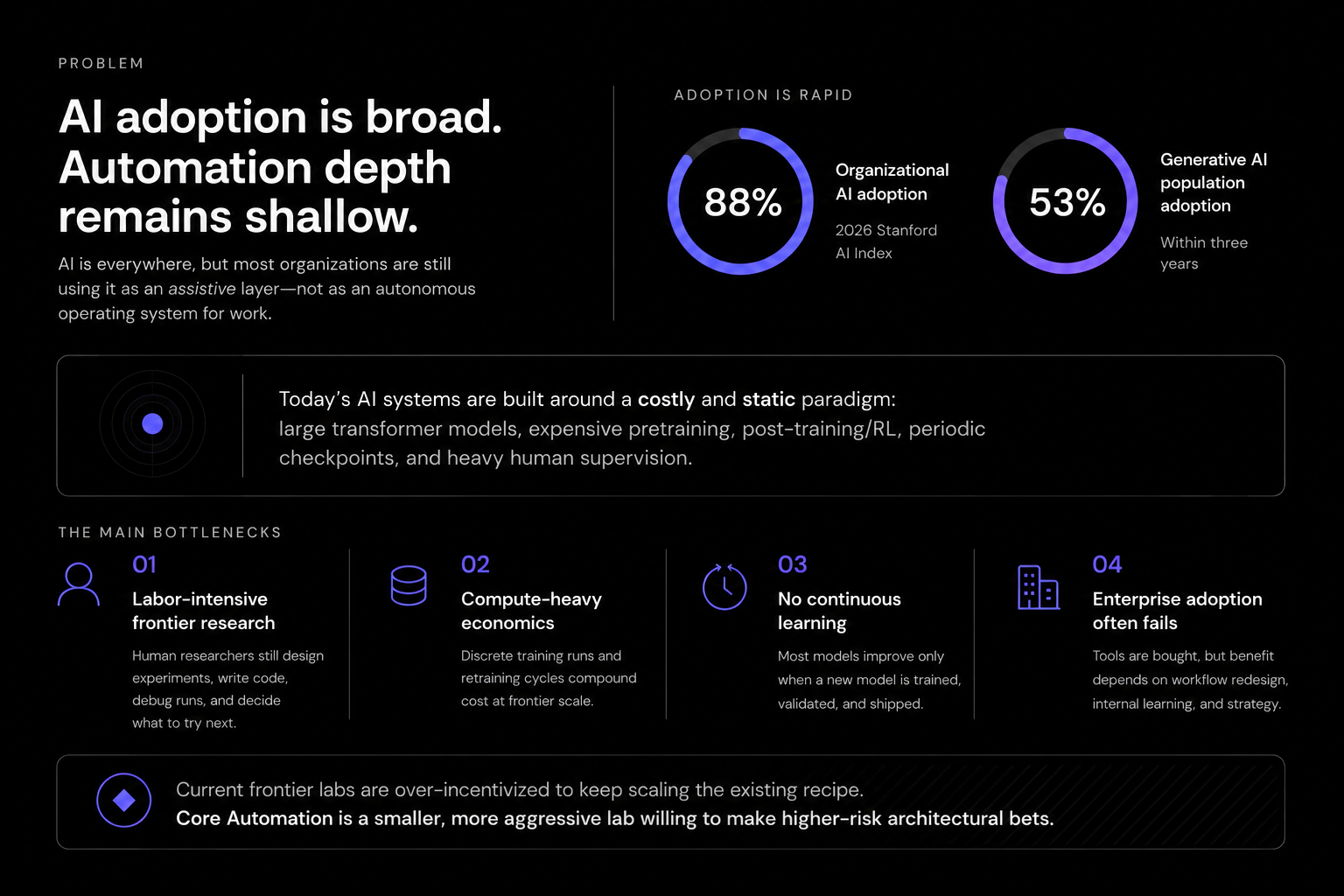

AI adoption is now broad, but automation depth remains shallow. The 2026 Stanford AI Index reports that organizational AI adoption reached 88%, while generative AI reached 53% population adoption within three years. Yet most companies are still using AI as an assistive layer rather than as an autonomous operating system for work.

The problem Core Automation is attacking is not simply “AI is not good enough.” It is that today’s AI systems are still largely built around a costly and static paradigm: large transformer models, expensive pretraining, post-training/RL, periodic checkpoint releases, and heavy human supervision. That paradigm has produced major progress, especially in coding, reasoning, and research assistance, but it leaves several structural bottlenecks:

Core Automation’s view is that current frontier labs are over-incentivized to keep scaling the existing recipe because it is legible, fundable, and predictable. The company is positioning itself as a smaller, more aggressive lab willing to make higher-risk architectural bets.

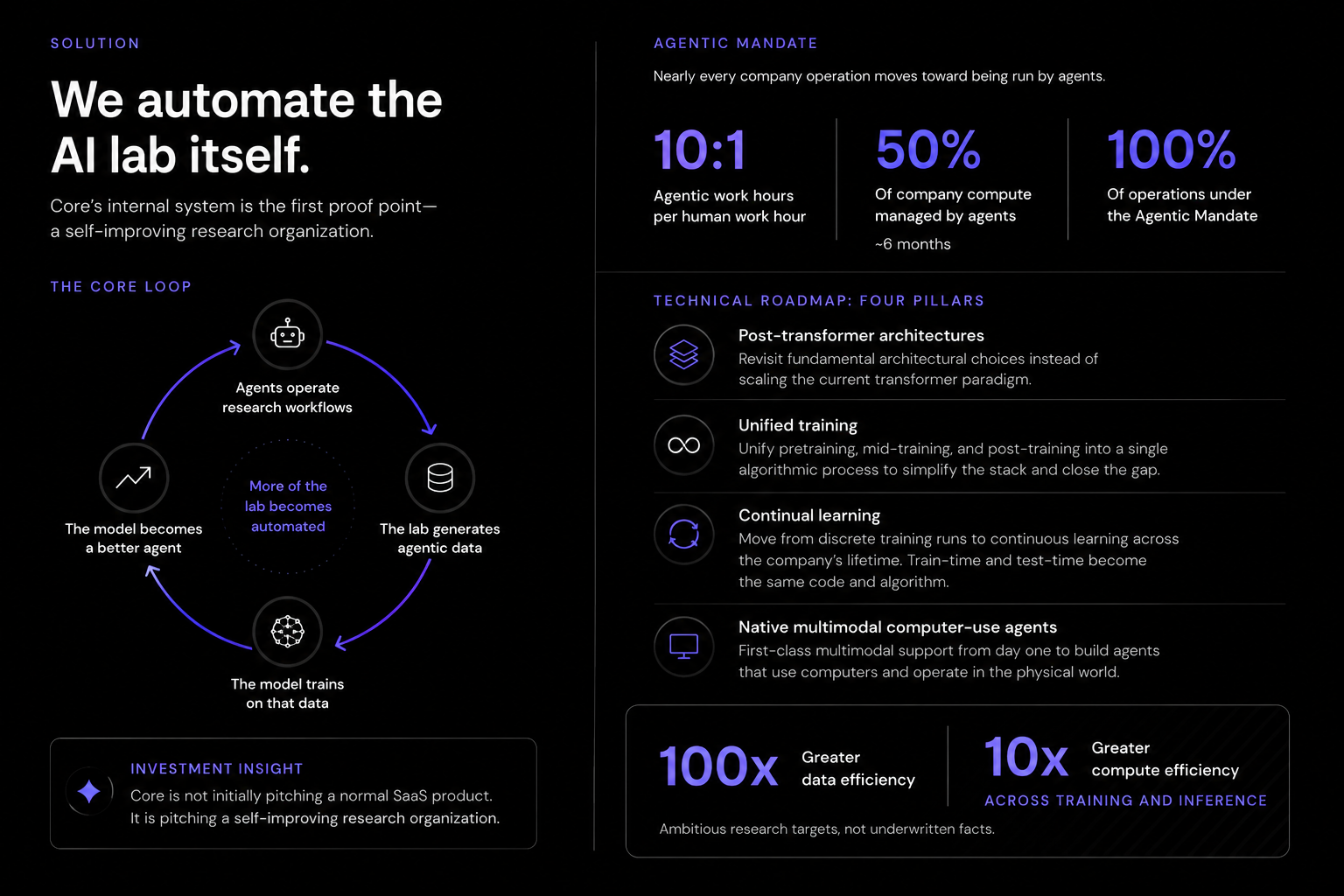

Core Automation’s solution is to automate the AI lab itself and use that internal system as the first proof point.

The company’s core loop is:

Agents operate research workflows → the lab generates agentic data → the model trains on that data → the model becomes a better agent → more of the lab becomes automated.

This is the key investment insight. Core is not initially pitching a normal SaaS product. It is pitching a self-improving research organization. The company’s internal “Agentic Mandate” requires that nearly every company operation move toward being run by agents. In the deck, Core targets 10:1 agentic work hours per human work hour, 50% of company compute managed by agents within roughly six months, and 100% of operations under the Agentic Mandate.

The technical roadmap has four main pillars.

The most ambitious claims in the company materials are 100x greater data efficiency and 10x greater compute efficiency across training and inference. These are potentially company-defining if achieved, but they should currently be treated as unproven research targets rather than underwritten facts.

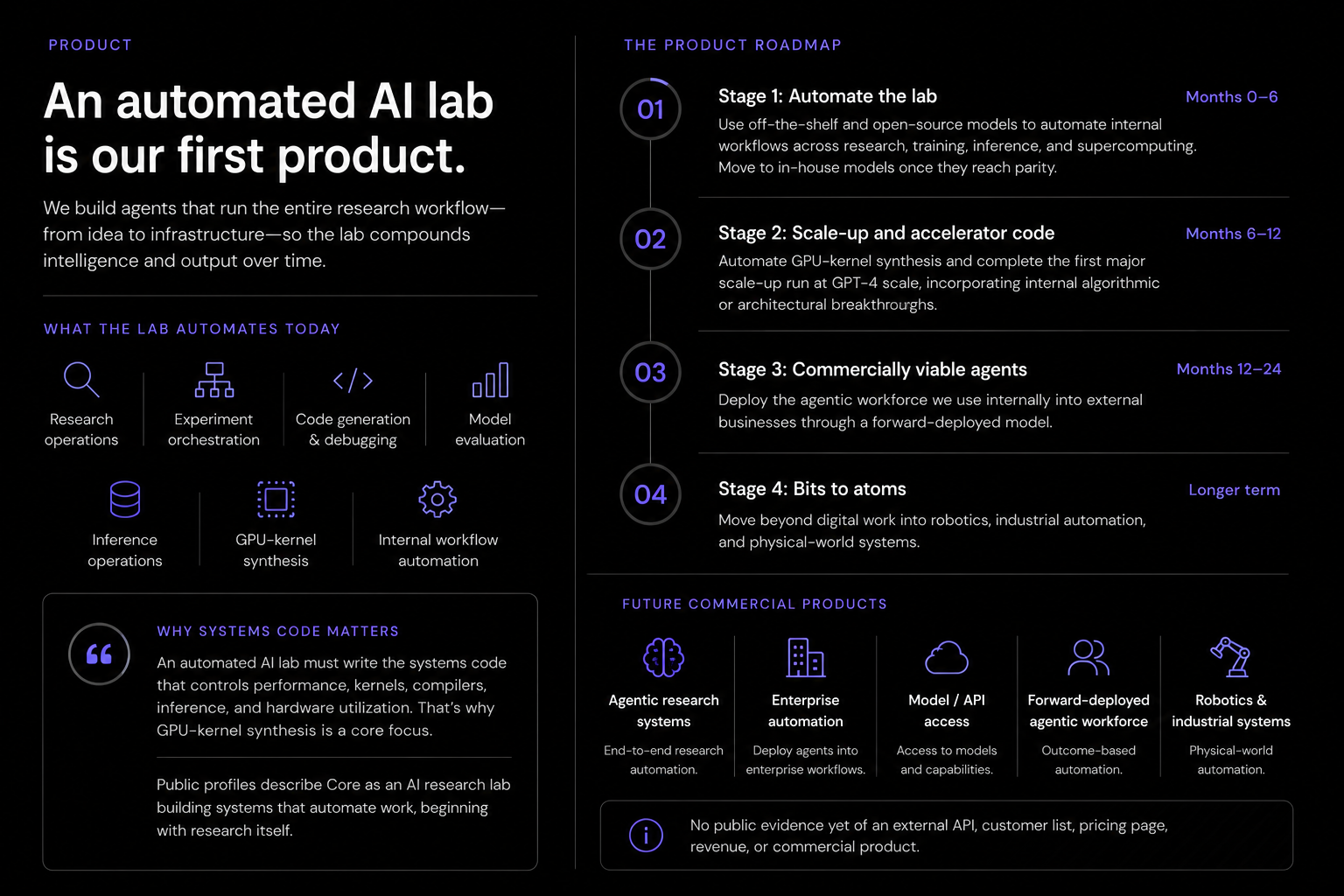

Core Automation is currently best understood as a research-lab-first company, not a commercial software company. Its near-term “product” is the automated lab itself: agents for research operations, experiment orchestration, model evaluation, code generation, debugging, inference operations, GPU-kernel synthesis, and internal workflow automation.

Core’s first public technical artifact is also directionally important. In “When AI Starts Writing Systems Code”, Mark Saroufim frames systems-code automation as a prerequisite for automating research itself. The point is that an automated AI lab cannot only automate high-level research reasoning; it must also automate the low-level code that controls performance, kernels, compilers, inference, and hardware utilization. This aligns with Core’s emphasis on GPU-kernel synthesis in the roadmap and gives the company a concrete early proving ground for its agentic research thesis.

Their product roadmap has four stages.

Their commercial products are agentic research systems, enterprise automation deployments, model/API access, forward-deployed agentic workforce solutions, and eventually robotics or industrial automation systems.

Talent Aggregation: Business Insider reported that Core recruited researchers from Anthropic and Google DeepMind and branded itself as the world’s most automated AI lab. It also cited Rohan Anil’s public post saying Jerry Tworek “nerdsniped” him into joining, and Anmol Gulati’s public statement that he was starting something new with exceptional people.

Capital & Compute. Dealroom reported that Core closed $100M at a $1B valuation and thet are now closing a further $400M. They have signed large compute deals which is a key bottleneck for many labs.

Technical Differentiation: Core’s blog post “When AI Starts Writing Systems Code”, and Mark Saroufim’s related MLSys keynote, frame systems-code generation as an early proving ground for AI-assisted research automation. This is relevant because systems code is hard to fake: it must satisfy performance, correctness, hardware constraints, and reproducibility.

Jerry Tworek, CEO. Former VP of reinforcement-learning research at OpenAI. He led the team that established the reasoning-model paradigm and oversaw a sequence of increasingly complex training runs. Business Insider identifies him as former OpenAI VP and CEO/cofounder of Core Automation.

Rohan Anil. Former Distinguished Engineer at Google DeepMind, co-led Gemini pretraining and PaLM 2, and most recently worked on pretraining research at Anthropic before joining Core.

Anmol Gulati. Former co-founder of Adept AI, led multimodal pretraining, worked on Project Mariner at Google DeepMind, and was first author of Conformer.

Dilip Krishnan. Former Senior Staff Research Scientist at Google DeepMind, with work across Gemini pretraining/post-training, reasoning, contrastive learning, multimodal representation learning, and generative models.

Ehsan Amid. Former Senior Research Scientist at Google Brain and Google DeepMind, core Gemini pretraining contributor, with expertise in robustness, optimization, architecture design, and representation learning.

Avery Lamp. Former DeepMind research engineer focused on agentic post-training, environments, and data; previously at MosaicML and Adept.

Mark Saroufim. Former PyTorch core maintainer at Meta; co-founder of GPU MODE; early work in kernel generation and competitive kernel programming.

Markus Hoehnerbach. Worked on PyTorch compiler at Meta and deep-learning systems at NVIDIA, including CUTLASS, cuTENSOR, TensorRT-LLM, cuEquivariance, and FlashAttention-related work.

Sağnak Taşırlar. Former Adept pretraining research engineer; PhD in computer science from Rice focused on parallel runtimes, compilers, and HPC.

Sai Surya Duvvuri. Researcher in data-efficient LLMs, long-context architectures, and optimization; prior roles at Microsoft Research, Google, DeepMind, FAIR, and IBM Research.

Swapnil Patil. Former Google engineer with 13+ years across accelerators, ML runtimes, Gemini/LLM performance, RDMA, and GPU systems.

Joanne Jang. Former General Manager and Head of Model Behavior at OpenAI; led product and model-behavior work across GPT-4, DALL·E 2, text-to-speech, the ChatGPT API, GPT-4o, GPT-4.5, and o3; founded OpenAI Labs.

Riley Walz. Software engineer and internet artist known for fast product execution and public-data projects, including Bop Spotter, Find My Parking Cops, and Jmail.

Julia Villagra. Former Chief People Officer at OpenAI and long-time Head of People at Hudson River Trading.

Francis Zhang. Former OpenAI inference engineer; according to the materials, contributed to GPT-4o and GPT-4.5 and led inference for later OpenAI models.

Kanav Garg. Former Google DeepMind/Gemini research engineer focused on RL data scaling and Project Mariner.

The team’s strength is not just individual pedigree. It is coverage across the full stack: algorithms, architectures, pretraining, post-training, agents, multimodal, inference, compilers, kernels, product, and people/culture. That breadth matters because Core’s thesis requires both fundamental research and extreme systems execution.

Core Automation’s market opportunity has three layers.

The largest upside case is that Core becomes not just an “agent company,” but a new foundational lab with better model economics.

Core competes across several categories.

Core’s advantage is talent density and willingness to take architectural risk.

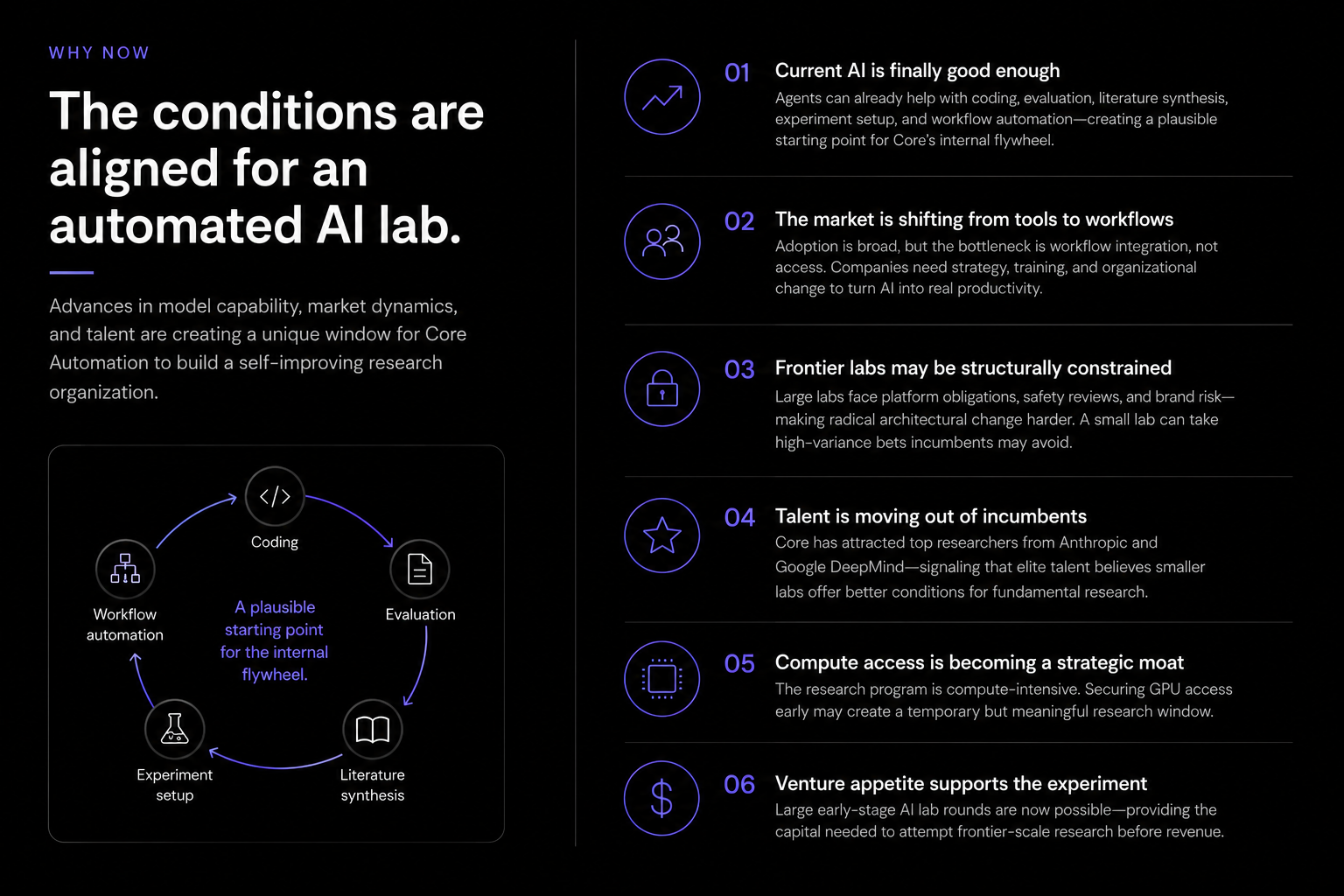

Current AI is finally good enough to automate parts of AI research. Agents are not fully autonomous, but they can already help with coding, evaluation, literature synthesis, experiment setup, and workflow automation. That creates a plausible starting point for Core’s internal flywheel.

The market is shifting from tools to workflows. Companies have adopted AI broadly, but the bottleneck is increasingly workflow integration rather than access. Business Insider emphasizes that companies need strategy, training, and organizational change to translate AI tools into actual productivity. Core’s thesis is directly aligned with this shift: it is not building another chatbot, but an AI-operated work system.

Frontier labs may be structurally constrained. Large labs have customers, revenue commitments, safety reviews, platform obligations, and brand risk. That makes radical architectural change harder. A small lab can take high-variance bets that incumbents may avoid.

Talent is moving out of incumbents. Core has reportedly attracted top researchers from Anthropic and Google DeepMind, which suggests that some elite researchers believe smaller labs offer better conditions for fundamental research.

Compute access is becoming a strategic moat. The capital raise is large because the research program is compute-intensive. If Core can secure GPU access early, it may have a temporary research window.

Venture appetite supports the experiment. Large early-stage AI lab rounds are now possible. This gives Core enough capital to make a serious attempt at frontier-scale research, even before revenue.

The company’s best argument is that the team is unusually well matched to the ambition: OpenAI reasoning/RL leadership, Gemini and PaLM pretraining, DeepMind and Adept agent experience, PyTorch/GPU systems, inference, model behavior & product.

The upside case is significant. If Core can automate its own research lab, it may produce more research output per person than much larger labs. If its continual-learning architecture works, it could create a new model category with better economics. If those systems commercialize, Core could become a major enterprise automation platform or a new foundational model company.

Round

$400M

Investors

Lightspeed, Menlo Ventures, Accel, Nvidia, CRV, Spark

Date

16 July

Questions

team@joinbeyond.coMemo

Core Automation is a highly credible AI “neo-lab” building “the world’s most automated AI lab,” starting by automating its own research workflows. Founded by former OpenAI VP Jerry Tworek, with senior talent from Anthropic, Google DeepMind, Adept, Meta, and Google, the team is very strong across reasoning models, pretraining, multimodal agents, GPU systems, inference, model behavior, and AI infrastructure.

Rather than building another AI application, Core is creating a self-reinforcing research engine where agents run workflows, generate training data, and improve the models operating the lab. If successful, this could allow a small, talent-dense team to compete with much larger frontier labs while pursuing breakthroughs in continual learning, post-transformer architectures, GPU-kernel automation, and more efficient training.

Core may represent the next phase of AI. While highly ambitious, this is the type of paradigm-shift bet that can define a generation of AI companies, similar in spirit to Anthropic: when Dario Amodei left OpenAI to build a frontier lab, an investment at a $3B valuation would have produced a return of over 300x.

AI adoption is now broad, but automation depth remains shallow. The 2026 Stanford AI Index reports that organizational AI adoption reached 88%, while generative AI reached 53% population adoption within three years. Yet most companies are still using AI as an assistive layer rather than as an autonomous operating system for work.

The problem Core Automation is attacking is not simply “AI is not good enough.” It is that today’s AI systems are still largely built around a costly and static paradigm: large transformer models, expensive pretraining, post-training/RL, periodic checkpoint releases, and heavy human supervision. That paradigm has produced major progress, especially in coding, reasoning, and research assistance, but it leaves several structural bottlenecks:

Core Automation’s view is that current frontier labs are over-incentivized to keep scaling the existing recipe because it is legible, fundable, and predictable. The company is positioning itself as a smaller, more aggressive lab willing to make higher-risk architectural bets.

Core Automation’s solution is to automate the AI lab itself and use that internal system as the first proof point.

The company’s core loop is:

Agents operate research workflows → the lab generates agentic data → the model trains on that data → the model becomes a better agent → more of the lab becomes automated.

This is the key investment insight. Core is not initially pitching a normal SaaS product. It is pitching a self-improving research organization. The company’s internal “Agentic Mandate” requires that nearly every company operation move toward being run by agents. In the deck, Core targets 10:1 agentic work hours per human work hour, 50% of company compute managed by agents within roughly six months, and 100% of operations under the Agentic Mandate.

The technical roadmap has four main pillars.

The most ambitious claims in the company materials are 100x greater data efficiency and 10x greater compute efficiency across training and inference. These are potentially company-defining if achieved, but they should currently be treated as unproven research targets rather than underwritten facts.

Core Automation is currently best understood as a research-lab-first company, not a commercial software company. Its near-term “product” is the automated lab itself: agents for research operations, experiment orchestration, model evaluation, code generation, debugging, inference operations, GPU-kernel synthesis, and internal workflow automation.

Core’s first public technical artifact is also directionally important. In “When AI Starts Writing Systems Code”, Mark Saroufim frames systems-code automation as a prerequisite for automating research itself. The point is that an automated AI lab cannot only automate high-level research reasoning; it must also automate the low-level code that controls performance, kernels, compilers, inference, and hardware utilization. This aligns with Core’s emphasis on GPU-kernel synthesis in the roadmap and gives the company a concrete early proving ground for its agentic research thesis.

Their product roadmap has four stages.

Their commercial products are agentic research systems, enterprise automation deployments, model/API access, forward-deployed agentic workforce solutions, and eventually robotics or industrial automation systems.

Talent Aggregation: Business Insider reported that Core recruited researchers from Anthropic and Google DeepMind and branded itself as the world’s most automated AI lab. It also cited Rohan Anil’s public post saying Jerry Tworek “nerdsniped” him into joining, and Anmol Gulati’s public statement that he was starting something new with exceptional people.

Capital & Compute. Dealroom reported that Core closed $100M at a $1B valuation and thet are now closing a further $400M. They have signed large compute deals which is a key bottleneck for many labs.

Technical Differentiation: Core’s blog post “When AI Starts Writing Systems Code”, and Mark Saroufim’s related MLSys keynote, frame systems-code generation as an early proving ground for AI-assisted research automation. This is relevant because systems code is hard to fake: it must satisfy performance, correctness, hardware constraints, and reproducibility.

Jerry Tworek, CEO. Former VP of reinforcement-learning research at OpenAI. He led the team that established the reasoning-model paradigm and oversaw a sequence of increasingly complex training runs. Business Insider identifies him as former OpenAI VP and CEO/cofounder of Core Automation.

Rohan Anil. Former Distinguished Engineer at Google DeepMind, co-led Gemini pretraining and PaLM 2, and most recently worked on pretraining research at Anthropic before joining Core.

Anmol Gulati. Former co-founder of Adept AI, led multimodal pretraining, worked on Project Mariner at Google DeepMind, and was first author of Conformer.

Dilip Krishnan. Former Senior Staff Research Scientist at Google DeepMind, with work across Gemini pretraining/post-training, reasoning, contrastive learning, multimodal representation learning, and generative models.

Ehsan Amid. Former Senior Research Scientist at Google Brain and Google DeepMind, core Gemini pretraining contributor, with expertise in robustness, optimization, architecture design, and representation learning.

Avery Lamp. Former DeepMind research engineer focused on agentic post-training, environments, and data; previously at MosaicML and Adept.

Mark Saroufim. Former PyTorch core maintainer at Meta; co-founder of GPU MODE; early work in kernel generation and competitive kernel programming.

Markus Hoehnerbach. Worked on PyTorch compiler at Meta and deep-learning systems at NVIDIA, including CUTLASS, cuTENSOR, TensorRT-LLM, cuEquivariance, and FlashAttention-related work.

Sağnak Taşırlar. Former Adept pretraining research engineer; PhD in computer science from Rice focused on parallel runtimes, compilers, and HPC.

Sai Surya Duvvuri. Researcher in data-efficient LLMs, long-context architectures, and optimization; prior roles at Microsoft Research, Google, DeepMind, FAIR, and IBM Research.

Swapnil Patil. Former Google engineer with 13+ years across accelerators, ML runtimes, Gemini/LLM performance, RDMA, and GPU systems.

Joanne Jang. Former General Manager and Head of Model Behavior at OpenAI; led product and model-behavior work across GPT-4, DALL·E 2, text-to-speech, the ChatGPT API, GPT-4o, GPT-4.5, and o3; founded OpenAI Labs.

Riley Walz. Software engineer and internet artist known for fast product execution and public-data projects, including Bop Spotter, Find My Parking Cops, and Jmail.

Julia Villagra. Former Chief People Officer at OpenAI and long-time Head of People at Hudson River Trading.

Francis Zhang. Former OpenAI inference engineer; according to the materials, contributed to GPT-4o and GPT-4.5 and led inference for later OpenAI models.

Kanav Garg. Former Google DeepMind/Gemini research engineer focused on RL data scaling and Project Mariner.

The team’s strength is not just individual pedigree. It is coverage across the full stack: algorithms, architectures, pretraining, post-training, agents, multimodal, inference, compilers, kernels, product, and people/culture. That breadth matters because Core’s thesis requires both fundamental research and extreme systems execution.

Core Automation’s market opportunity has three layers.

The largest upside case is that Core becomes not just an “agent company,” but a new foundational lab with better model economics.

Core competes across several categories.

Core’s advantage is talent density and willingness to take architectural risk.

Current AI is finally good enough to automate parts of AI research. Agents are not fully autonomous, but they can already help with coding, evaluation, literature synthesis, experiment setup, and workflow automation. That creates a plausible starting point for Core’s internal flywheel.

The market is shifting from tools to workflows. Companies have adopted AI broadly, but the bottleneck is increasingly workflow integration rather than access. Business Insider emphasizes that companies need strategy, training, and organizational change to translate AI tools into actual productivity. Core’s thesis is directly aligned with this shift: it is not building another chatbot, but an AI-operated work system.

Frontier labs may be structurally constrained. Large labs have customers, revenue commitments, safety reviews, platform obligations, and brand risk. That makes radical architectural change harder. A small lab can take high-variance bets that incumbents may avoid.

Talent is moving out of incumbents. Core has reportedly attracted top researchers from Anthropic and Google DeepMind, which suggests that some elite researchers believe smaller labs offer better conditions for fundamental research.

Compute access is becoming a strategic moat. The capital raise is large because the research program is compute-intensive. If Core can secure GPU access early, it may have a temporary research window.

Venture appetite supports the experiment. Large early-stage AI lab rounds are now possible. This gives Core enough capital to make a serious attempt at frontier-scale research, even before revenue.

The company’s best argument is that the team is unusually well matched to the ambition: OpenAI reasoning/RL leadership, Gemini and PaLM pretraining, DeepMind and Adept agent experience, PyTorch/GPU systems, inference, model behavior & product.

The upside case is significant. If Core can automate its own research lab, it may produce more research output per person than much larger labs. If its continual-learning architecture works, it could create a new model category with better economics. If those systems commercialize, Core could become a major enterprise automation platform or a new foundational model company.